2

Costs, Benefits, and Value: Context, Concepts, and Approach

This chapter outlines the Committee’s approach to identifying the costs and lost value consequent to uninsurance and to estimating the resources that would be needed to bring the utilization of health care among the uninsured population in the United States in line with that of those with coverage. The Committee builds upon its earlier work. Its findings in previous reports both establish the context for and serve as points of departure for the analysis of costs and benefits presented here. The following are several of the important insights gained from the Committee’s earlier work:

-

Health insurance is more than a mechanism for spreading financial risks; it also promotes appropriate use of preventive and routine health care services that otherwise may be underutilized (IOM, 2002a,b).

-

Uninsurance is not usually voluntary; most individuals and families that lack coverage do so because they do not have a workplace offer or cannot afford the coverage available to them (IOM, 2001a).

-

The lack of health insurance by some has adverse spillover effects on those with health insurance (IOM, 2002b, 2003a).

-

The prevalence of uninsurance sits uneasily beside the favorable tax treatment of employment-based health insurance and the health insurance programs of the Social Security Act (Medicare, Medicaid, and the State Children’s Health Insurance Program [SCHIP]), which are funded by federal income and payroll taxes and broad-based state taxes (IOM, 2001a, 2003a).

These aspects of health insurance and the role it plays in the American health care enterprise and the economy more broadly, and its potential impacts on social and

political culture, shape the discussion of the costs of uninsurance throughout this report.

This chapter defines and exemplifies the kinds of costs that the Committee considers.1 Some of these are quantified and expressed in monetary terms, some have not been quantified because the data and analyses needed for quantification are not available, and some have no ready monetary equivalents.

The first section sets out the context for the analysis of costs, benefits, and value presented in the report, including the conceptual framework that has guided the Committee’s work in its previous reports. The second section presents definitions and a categorization scheme for the types of costs referred to throughout the report. The third section describes the Committee’s approach to determining the costs of uninsurance and the costs and benefits of coverage. Finally, the last section reviews the limitations of the Committee’s analysis and of the data and research base used to evaluate these costs and benefits.

ANALYTIC CONTEXT

This section (1) explains the Committee’s reasons for adopting the societal perspective in this report and what that perspective entails, (2) reviews the conceptual framework that has guided the Committee’s assessment of the consequences of uninsurance, and (3) considers the features of health insurance that account for its value as an economic and social good and thus illuminate the costs incurred when all members of society do not have it.

The Societal Perspective

In this report the Committee explicitly takes a broad societal perspective in assessing the performance of the private and public economic resources devoted to health care, health insurance, and alternative uses for these resources. These resources include family resources, firms’ investments, and tax revenues. This perspective dictates that the Committee’s calculus take into account costs and outcomes beyond those that accrue to economic actors such as individuals, families, and firms as evaluated by these actors individually (Culyer, 1991; Weinstein and Manning, 1997). Health care is valued highly and widely throughout American society. Providing health care to those who need it not only expresses compassion and norms of mutual assistance, but it is also a form of social and political recognition. In the Committee’s analysis, the societal perspective implicitly incorporates an assessment of the fairness of the distribution of these costs and benefits across individuals, as members of one national community, as taxpayers, and as business owners because it accounts for all health effects and costs that flow from a particu-

|

1 |

In this chapter, terms used in a technical sense are printed in italics the first time they appear, and can be found in the Glossary in Appendix A. |

lar intervention (e.g., health insurance coverage) regardless of who would experience these effects.

In adopting the societal perspective, the Committee follows the guidance of the Panel on Cost-Effectiveness in Health and Medicine, a nonfederal panel convened by the U.S. Public Health Service that developed consensus-based recommendations for guiding the conduct of cost-effectiveness analysis in health and medicine. The objective of the Panel was to improve the comparability and quality of studies that inform the allocation of health care resources. The Panel argued for adopting the societal perspective because it represents the public interest rather than the particular interest of any one group within society. It also argued that adopting the societal perspective was a practical choice that provides a benchmark against which more particularistic perspectives (e.g., those of employers or population subgroups such as young adults) can be evaluated:

If an employer adopts an intervention that reduces the employer’s health insur-ance costs but increases costs for Medicare, or if a public health intervention improves the health of one group but causes unwanted side effects for another, the societal perspective includes both changes. No perspective has a stronger claim to be the basis for comparability across studies (Russell et al., 1996, p. 1174).

Conceptual Framework for Identifying Consequences ofUninsurance

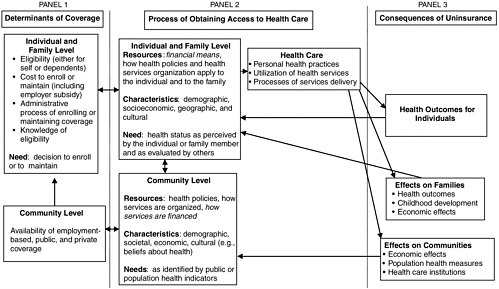

The Committee’s investigation, as presented in its previous four reports, has been guided by an overarching conceptual framework introduced in Coverage Matters (IOM, 2001a). This conceptual framework adapted a widely applied behavioral model of access to health care, developed by Aday and colleagues (1984) and more recently presented in Andersen and Davidson (2001). In summary, the model posits and illustrates how individual and social factors, that is, both individual and community-level characteristics and resources, affect receipt of health care and how individual, familial, and community health, financial, and social outcomes follow from the extent and nature of the care received. The outcomes, which ultimately result from individual health insurance status and coverage rates within communities, cascade from the individual and family to the community level. Figure 2.1 illustrates the conceptual framework, and the right side of the diagram includes the three main consequences of uninsurance examined in this report:

-

The economic costs (worse health, developmental, and functional out-comes for children and adults) that result from their lack of health insurance;

-

The impact on family economic stability and psychosocial well-being when any member of a family lacks coverage;

-

The spillover effects within communities of relatively high uninsured rates on health care services and institutions, local economies, and population health.

The costs and consequences of uninsurance are, conversely, the potential benefits of universal health coverage. Where possible, the Committee describes the lost value due to uninsurance in monetary terms. The report also considers the lost economic value and social and political opportunities that have not been or cannot be quantified in monetary terms, including the realization of social values and ideals like equality of opportunity, social and political equity, and mutual concern among members of a local community or the national polity.

Health Insurance as an Economic and Social Good

In order to appreciate the costs associated with the absence of health insur-ance, it is important to understand why and how we, both as consumers and as citizens, value coverage. Americans have long considered health care to be both a market commodity and a social good, a view that has fostered the development of variegated and complex arrangements for the delivery of health care (Fuchs, 1996; IOM, 2001a). This dual identity of health insurance as both a market good and a social good is reflected in the Committee’s two-part analysis in this report; the analysis is both positive and empirical, and normative.

Health insurance provides financial protection against uncertain and potentially catastrophic health expenses and also facilitates access to health care services (IOM, 2001a). In the early 20th century in the United States, a private market in health insurance developed concurrently with the increasing cost and increasing effectiveness of medical care and, in the 1960s, continued alongside governmental social insurance programs such as Medicare and Medicaid.2 The benefits of health insurance (private and public) and charity care are distinct but overlap. Both health insurance and charity care provide financial protection and access to collectively and individually valued health services when individuals fall ill. Additionally, private and public coverage afford enrollees some degree of peace of mind in the knowledge that care that might be needed at some future time will be accessible and affordable.

The following discussion compares and contrasts the features and aspects of value of private health insurance and public coverage through social insurance and social welfare programs.

Private Health Insurance

Private group and individual health insurance are like other kinds of insurance (e.g., fire, accident) in that they protect against financial catastrophes resulting from bad luck; health insurance mitigates the financial burdens of being sick.

Unlike with other kinds of insurance, however, most health insurance policy holders can expect to make claims against their policies.3 Individuals and policy makers also value health insurance because it facilitates access to services that promote health, such as preventive measures and screening, in addition to those that remedy illness and injury. Health insurance also offers its enrollees the advantages of realizing economies through group purchasing and improving information about health services and providers. Thus health insurance has value beyond that entailed by most other kinds of risk insurance.

Private health insurance, by pooling the risks of many individuals, can improve the economic efficiency with which a fixed amount of resources, namely, the dollars that a group of people could devote either to medical care or health insurance, is spent. The utility or welfare of the individuals contributing to the insurance pool is greater than it would be if each retained their premium dollars and faced uncertain and risky health expenses. Health insurance premiums incorporate a loading fee, a charge above the actuarial value of the benefits provided that includes an allowance for risk (the risk premium), administrative costs, and profit. The larger the group, the smaller the loading fee per capita, because of economies of scale both in administrative costs and in the risk premium, because the variance in expected expenditures decreases as the size of the group whose risks are pooled increases. Premiums for private health insurance must reflect average spending by enrollees, so in most years, people get back less than the full premium payment, but those with major illness benefit from coverage of expenses that may be well in excess of their annual income.

One feature of insurance that affects the operation and costs of health coverage is moral hazard, a term coined by the insurance industry to describe increases in the use of insured goods or services because covered individuals are not directly or fully financially liable when they use services. Physicians and other providers of services also respond to insurance coverage by offering and providing more services than they would otherwise. Low out-of-pocket costs for insured health care result in people getting more care than they would have if they had to pay the full costs out of pocket.

Much of this increased utilization is desirable. Preventive and screening services, for example, are used more frequently and appropriately by the insured than by those without health insurance (IOM, 2002a,b). Insured people are less likely than uninsured people to delay seeking care for potentially serious conditions (Baker et al., 2001). Delayed care is often more expensive and less effective. The differences in use of services between insured and uninsured individuals is reported in Chapter 3, and evaluated in monetary terms in Chapter 5.

Some of the additional medical attention and treatment that insured people

receive, however, may be worth less than their total costs or even harmful (IOM, 2001b). The increases in premiums due to incurred costs that are not highly valued result in a welfare loss for those purchasing the insurance (Currie and Madrian, 1999). Because enrollees would not want or be able to pay the premiums that would result if all care were free and without restrictions, health insurance is structured to limit the use of care through patient cost sharing (deductibles, copayments and coinsurance), provider payment arrangements like capitation, and administrative mechanisms like prior authorization.

Recent work in the theory of demand for health insurance has led to a reconsideration of the extent of welfare losses resulting from “too much” health insurance (de Meza, 1983; Nyman, 1999a,b). This theoretical work assumes that people value certain kinds of (costly) health care more when they are sick than when they are well. Because we do not know with certainty what our health will be in a future time period, we tend to pay a lot to ensure that, if we turn out to need or be able to benefit from such (costly) health care, it is available to us then (Glied and Remler, 2002).

In addition to costs of care following acute crises to apparently healthy people, such as a heart attack or a car crash, other health care costs are predictably larger for some people, such as those with one or more chronic conditions. Insurance is particularly valuable to such people and they are more likely to try to obtain more extensive coverage than those who do not anticipate using the benefits. This phenomenon is called adverse selection. Individual insurance is particularly likely to be subject to adverse selection because those who are willing to pay the full premium out of pocket have health-related reasons for valuing it highly. Insurance companies anticipate this adverse selection for individual policies and attempt to limit their liability through medical underwriting, exclusions of preexisting conditions from coverage, high loading, and generally less extensive benefits for premiums (Chollet and Kirk, 1998; Pauly and Percy, 2000).

Insurance offered through large employer groups is less subject to adverse selection because there is a large pool of insured people who have come together for some purpose other than to obtain coverage. Employees are also more likely to elect workplace health insurance because it is tax subsidized and comes with the job rather than because they perceive an immediate need for it. In most large companies, employees with the same type of coverage pay the same out-of-pocket premium. (The full premium price negotiated for the group overall will likely reflect at least the age and gender composition of the workforce and, if available, prior years’ claims experience.) When someone (a worker or the worker’s dependent) who has group-based health insurance develops a potentially costly health condition, the worker may be particularly reluctant to leave her job because the job-related health insurance has become particularly valuable and health insurance may not be obtainable or affordable either individually or through another employer. This tendency to stay with a job when it is no longer the optimal work situation because of a health benefit that might not be available elsewhere at a

comparable price introduces an inefficiency in the labor market referred to as job lock (Madrian, 1994).

The private individual and group health insurance markets in the United States fail to offer policies to all who might want coverage, and there are only limited regulatory consumer protections for maintaining private coverage once someone has it. First in 1985, with the Consolidated Omnibus Budget Reconciliation Act (COBRA), and again in 1996 with the Health Insurance Portability and Accountability Act (HIPAA), Congress enacted statutory measures to help individuals who have coverage continue it after leaving or losing their jobs. Still, all Americans, except those who turn 65 and qualify for Medicare on the basis of age or those who have end-stage renal disease (and thus also have Medicare lifelong), are at risk for being without health insurance at some point in their lives (IOM, 2001a, 2002b). While state regulation of health insurance and the creation of high-risk pools in some states have attempted to improve the availability of policies for those in poor health, these efforts are limited and have not resulted in sufficient access to affordable insurance (Chollet, 2000; Nichols, 2000; Pauly and Percy, 2000).4 Government programs have filled some of the gaps, particularly programs such as Medicare and Medicaid, which provide health care through insurance mechanisms to identified populations with an entitlement to specific services.

Public Coverage

Health benefits are provided publicly through both social insurance and social welfare programs. Social insurance programs typically operate through public taxation and public spending. Social insurance programs can be distinguished from social welfare programs through features such as mandatory contributions, benefits from earmarked sources or funds, qualification for benefits under a uniform set of rules, and a perception by beneficiaries that they have earned or are entitled to benefits (NASI, 1999). In market-based economies, social insurance programs contribute to social stability by providing some degree of economic security by spreading certain kinds of risks broadly across society (Dionne, 1998; NASI, 1999).

The motivations for extending social insurance and social welfare benefits to specific groups within the population or to all members of a society or nation differ by the type of good or benefit provided (e.g., health care or income), among countries (and states within the United States) and by beneficiary group (children, retired persons, citizens). In the United States, the federal government provides health benefits through Medicare and, along with the states, through Medicaid

and SCHIP to people for whom private health insurance markets do not exist or do not work well (the disabled and elderly) or who cannot afford premiums or health services (children and parents in low-income families, low-income disabled and elderly adults).

Medicare was enacted in 1965 to relieve the elderly and their families of the financial burden of catastrophically high medical care expenses, in the face of an inadequate and failing private market for individual health insurance for retirees. Medicaid was enacted at the same time to ensure that women and children receiving income support (and very low-income elderly and disabled persons) had access to needed health care, which included screening, prevention, and treatment of childhood diseases and developmental conditions after 1967. Beginning in the mid-1980s and culminating with the enactment of SCHIP in 1997, a series of expansions in Medicaid income-eligibility standards for pregnant women and children emphasized the public and national interest in and responsibility for investing in healthy starts for infants and children (see IOM, 2002b, for a fuller discussion of these expansions).

In 1994, vaccines for children (VFC) also became an entitlement for uninsured, Medicaid-enrolled, and other lower-income and underinsured children as part of Title 19 of the Social Security Act, a notable broadening of the Medicaid statute (Johnson et al., 2000; Rosenbaum, 2000). The motivation for and commitment to providing public support for children’s health coverage include both the recognition by federal and state legislators that children are a particularly vulnerable population who would suffer great harm over their lifetime without adequate health care and that the health and optimal development of children is an investment in the nation’s human capital, just as is public investment in their primary and secondary education.

Summary

Whether provided through the private individual and group markets or as public benefits, health insurance coverage is inherently a collective good, valued because it increases individual and collective well-being in a number of distinct ways. It is one aspect of contemporary social and economic life by which we share in each other’s fates in important ways and reduce the exposure to health and financial risks that each of us would otherwise face alone.

CONCEPTS OF COST

“Cost” has both everyday and more technical meanings. Without further specification, in some contexts its meaning is ambiguous. In this report, unless otherwise noted, a “cost of uninsurance” refers to an economic cost, the value of resources devoted to a given activity measured by their value if deployed elsewhere, also called the opportunity cost of the resources (Dranove, 1995). Economic costs can be incurred without explicit payments being made. Economic costs are

distinguished from cost or money transfers, which do not reflect an increase or decrease in economic cost or value but rather a redistribution of resources between individuals or other economic agents. For example, Social Security Disability Insurance payments to beneficiaries are a transfer of resources from the federal program (from taxpayers’ dollars) to entitled and enrolled individuals. This is sometimes referred to as a “program cost,” but the transfer payment itself is not an economic cost.

This report categorizes costs under two additional typologies, health services costs and other costs, and internal (private) costs and external (societal) costs. The costs of health care services that those without health insurance use do not, for the most part, represent economic costs attributable to being uninsured. The level of per capita expenditures for those without coverage is important, however, for measuring the difference in health care costs and utilization between otherwise similar insured and uninsured populations. Furthermore, the distribution of these costs among payers and sponsors of uncompensated care is also important. Figure 2.2 presents a matrix of these categories, and locates the particular elements of economic costs and transfers within its cells. Costs that are transfers are noted in the figure. The remainder of the section describes the classifications.

Cost-of-illness studies, which estimate the total value of resources expended as a result of the incidence or prevalence of a particular health condition, typically distinguish direct medical costs incurred from other costs, such as losses of productivity and premature death. The Committee follows this general distinction in the organization of the remaining chapters. Chapter 3 considers the health care services expenditures made on behalf of uninsured individuals. Chapter 4 considers the other, non-health care costs incurred as a result of an uninsured population. Chapter 5 presents estimates of the health care resources that would be needed if the uninsured were to receive the same kind and amount of health care that those with insurance use.

This report also distinguishes economic costs that are borne privately by individuals, families, and particular firms (internal costs) from those that “spill over” and affect others in the society or economy (external costs). Following Manning and colleagues (1989, 1991), the total social costs of an individual behavior (such as smoking) or a condition (such as having tuberculosis or being uninsured) can be categorized as internal and external costs. Internal costs include the costs of medical services resulting from the behavior or condition for which the individual pays, lost earnings that result from poorer health, and other out-of-pocket expenses incurred as a result of the behavior or condition. The poorer health and reduced longevity associated with being uninsured is an internal cost of uninsurance because it affects the uninsured individual. Conversely, the incremental value of the better health status and longer life expectancy of that same individual if insured is an internal or private benefit of providing health insurance.

External or spillover costs are the costs imposed on others by the behavior or condition. An external cost of an untreated case of tuberculosis, for example, includes the infection of others with the disease. The costs of uncompensated care

|

|

Internal Costs (for individuals, families, and firms) |

External Costs (to society) |

|

Health Care Service Costs |

• Out-of-pocket expenditures for health care services |

• Expenditures for uncompensated care (primarily transfer costs) |

|

Other Costs |

• Greater morbidity and premature mortality • Developmental losses for children • Diminished sense of social equality and of self-respect • Family financial uncertainty and stress, depletion of assets (resource and transfer costs) • Lost income of uninsured breadwinner in ill health • Workplace productivity losses (absenteeism, reduced efficiency on the job) |

• Diminished quality and availability of personal health services • Diminished public health system capacity • Diminished population health (e.g., higher rates of vaccinepreventable disease) • Higher taxes, budget cuts, loss of other uses for public revenues diverted to uncompensated care (primarily transfer costs) • Higher public program costs connected with worse health (e.g., Medicare, disability payments) (primarily transfer costs) • Diminished workforce productivity • Diminished social capital; unfulfilled social norms of caring, equal opportunity, and mutual respect |

FIGURE 2.2 Classification of the costs consequent to uninsurance.

borne by providers of services and taxpayers are external costs (transfers) of an individual’s uninsured status. The external costs associated with uninsurance include not only aggregated individual-level costs such as uncompensated care proximately borne by providers, but also community-level costs, such as the impact of relatively high uninsured rates on local hospitals and primary care providers and

the local economy generally. The costs discussed in Chapters 3 and 4 include both internal and external (resource and transfer) costs of uninsurance. Chapter 5, which projects the incremental utilization and resources that would be required if those without coverage used services as does the insured population, does not attempt to identify how these incremental costs would be distributed between the uninsured themselves and others.

APPROACH TO ESTIMATING THE COSTS OFUNINSURANCE AND THE COSTS AND BENEFITS OF COVERAGE

The methodological considerations that are important for the analyses pre-sented in this report differ from those of the Committee’s earlier work. The Committee established the nature of and, in some cases, estimated the probable magnitude of a number of health, financial, and institutional consequences of uninsurance in the earlier reports. This section outlines the Committee’s approach to calculating and aggregating the economic value of these effects, and describes and gives the rationale for the approach taken. Whenever possible, the Committee has relied on consensus recommendations (such as those of the Panel on Cost-Effectiveness in Health and Medicine mentioned earlier) in the treatment and reporting of costs and benefits and on analytic practices in cost-effectiveness and cost-benefit studies in health care and cost-of-illness studies.5

The relative merits of cost-effectiveness and cost-benefit analysis continue to be the subject of lively methodological and philosophical debates. The Committee has drawn from each of these approaches to examine the issue of the value of insurance for the uninsured from a variety of perspectives and to gain insight from each.

The remainder of this section describes (1) the analytic structure within which the Committee developed its estimates of the value of health forgone as a result of the lack of coverage and (2) the resources that would be needed to provide the currently uninsured population with the amount and kind of health care that those with either public or private coverage now use. It is important to keep in mind that imputing a monetary value to the reduced health and life expectancy that accompanies being uninsured is a different kind of analytic exercise from the calculation of actual expenditures incurred (or projected to be incurred) by or on behalf of those who lack coverage.

Estimating the Value of Longer Life and Improved Health

As a polity and a society, we make decisions about the economic value of life all the time in evaluating health and safety risks and the costs of reducing those risks. Being uninsured likewise can be thought of in terms of the risks of poorer health and shorter life faced by those without coverage (IOM 2002a,b). The Committee has posed the following question: How much health is lost within the U.S. population due to the lack of universal health insurance coverage? Conversely, what is the value of the increased health across the population that would be gained if those without health insurance coverage were to gain it, across the board? To answer these questions, the Committee adapted a common approach used in government rulemaking on health, safety, and environmental issues to determine the value of the difference in health outcomes, morbidity and mortality, that can be attributed to health insurance status.

Economists have used evidence of actual marketplace transactions that involve implicit tradeoffs between risk and money to estimate the value of a statistical (i.e., not identifiable) life (VSL) (Viscusi and Aldy, 2002). Such estimates have been used by governmental regulatory agencies such as the Environmental Protection Agency (EPA), the Food and Drug Administration, the Consumer Product Safety Commission, and the Department of Transportation. In conducting costbenefit analyses to guide regulation and investment in health and safety, these agencies, under the guidance of the Office of Management and Budget, have developed their own valuation methodologies and used a variety of approaches (OMB, 2003). The study included as Appendix B reviews these approaches in greater detail and justifies using a mid-range value of a statistical healthy year of life ($160,000) that corresponds to an average lifetime value of $4.8 million (Vigdor, 2003). Box 2.1 illustrates the application of this kind of analysis in the development of EPA regulations that set emissions standards for trucks and buses under the Clean Air Act (USEPA, 2001).

Health Capital and Human Capital

Health capital can be understood as the present value of the stock of health that an individual is expected to have over the course of his or her future lifetime. This concept is derived from the earlier notion of human capital, which posits that an individual’s stock of knowledge raises his or her productivity in the market sector of the economy and also in the nonmarket or household sector (Becker, 1964; Grossman, 1972; Cutler and Richardson, 1999). Analogous to education in the human capital model, an investment in health care in the health capital model adds to one’s stock of health, increasing time spent in a healthier state than otherwise.

Both human capital and health capital are analytic constructs based on the concept of personal utility in welfare economics. Each can be converted into monetary terms. The value of an individual’s stock of human capital is often expressed as the discounted present value of future earnings as a function of

|

BOX 2.1 An Example of Evaluating Costs and Benefits: Regulations for Clean Air and Vehicle Emissions Standards Federal agencies are required to evaluate the costs and benefits of regulations that have costs of at least $100 million. This information is part of the regulatory impact analysis that the Environmental Protection Agency (EPA) conducted prior to issuing new vehicle emissions standards. In 2001, EPA issued air pollution control rules to reduce emissions of particulate matter and nitrogen oxides from new heavy-duty trucks and buses by at least 90 percent below current standard levels by 2030 (USEPA, 2001).1 These standards require not only engine-based technology changes, but also diesel fuel production requirements to reduce fuel sulfur content by 97 percent. The engine manufacturing and refining changes imposed by the regulation are expected to have an aggregate annual economic cost of just over $3 billion in 2007, rising to $4.2 billion annually by 2030 (all values in 1999 dollars) (USEPA, 2001). When fully in place (2030), the new standards will reduce emissions of nitrogen oxides, nonmethane hydrocarbons, and particulate matter by a projected 2.6 million tons, 115,000 tons, and 109,000 tons, respectively, each year. The cleaner air that will result from these emissions controls is expected to avoid 8,300 premature deaths among adults aged 30 and older each year, 5,500 cases of chronic bronchitis, and 9,600 hospitalizations for respiratory or cardiovascular reasons. These health outcomes account for over 90 percent of the health and productivity gains of more than $70 billion annually that EPA estimates would be achieved with reduced emissions and improved air quality under the new standards for heavy engines and diesel fuel (USEPA, 2001). EPA used $6.1 million as the value of a statistical life for the purposes of these health benefits estimates. |

educational attainment, something that is easily calculated. Sometimes the value of nonmarket or household production is incorporated into the total value of human capital.

Estimating the value of a healthy life using human capital methods has two major problems. First, people value healthy life years for more reasons than their ability to earn income (Cutler and Richardson, 1997, 1999). Second, this approach values individuals’ lives differently depending on their education and income-producing potential, which violates widely held ethical and political principles of valuing the lives of all members of a democratic society alike. Although this second objection could be addressed by imputing the national mean or median human capital estimate to everyone, the first objection cannot be overcome. The Committee judged that the health capital approach better reflected the demonstrated value placed on better health and longer life.

Health capital takes into account people’s valuing of their own lives beyond

their ability to be productive and earn income over their working lifetime. The health capital approach, however, can be misleading because it is based on workers’ or consumers’ revealed preferences through their choices in the marketplace for small changes in the risks to their health and safety that they face. Although people are willing to pay substantial amounts for small reductions in risk, by buying smoke detectors or bicycle helmets (even if not required to by law), because of limits on their income they would not be able to “scale up” these amounts for slightly better health and safety in a statistical sense to the value equivalent that represents the value of their entire remaining life. It thus appears that people cannot “afford” their own lives, in the sense of being able to “pay” for the value ascribed to life through earnings capacity. At the same time, valuing life at more than earnings capacity has contributed to public policy decision making over the past 30 years and is based on empirical evidence of consumers’ implicit willingness to pay to reduce risks to life and health. Approaches using revealed preferences (through market transactions) can be contrasted with stated preferences approaches like contingent valuation, which is a survey-based approach to eliciting individuals’ preferences and priorities, described further below.

Valuing life at more than earnings capacity is consistent with how individuals and society as a whole make decisions. When insured people get seriously sick, they expect their insurance to pay substantial amounts if necessary, to purchase services that can provide a cure or ease their symptoms (de Meza, 1983; Nyman, 1999a,b). These amounts are often more than the insured could afford, sometimes many times more than their income. Pooled across many individuals through insurance, these costs are affordable. Analyzed as costs per life saved or compared to the improved quality of life they purchase, they generate estimates comparable to those used in the health capital analysis we present.

The remainder of this section reviews the metrics of health-related quality of life and quality-adjusted life years, which the Committee has employed in its analysis of health capital. These metrics are frequently used in clinical medical research and public health analysis to evaluate the effectiveness of particular health care interventions.

Valuing Different Health Outcomes

Converting the multiple dimensions of health status into a single metric that reflects the quality of life associated with a particular health profile poses a formidable challenge for economic and policy analysts. Health outcomes can be characterized more or less precisely and specifically. The most basic distinction in states of health is between being alive and being dead. The measure of premature mortality provides information about a determinant of health outcomes in terms of death prior to achieving an expected lifespan. The metric of years of life (YOL) lost converts this all-or-nothing measure of premature deaths into a proportionate measure, but one that is relatively crude. Health has many dimensions: physical, psychological, social, and functional.

One widely accepted scale measure of health status that attempts to build in these dimensions of health is the quality-adjusted life year (QALY) (Patrick and Erickson, 1993; Gold et al., 1996a). QALYs combine the length of life and the health-related quality of life (HRQL) that can be attributed to a given health state (CDC, 2000). QALY values or weights are derived empirically by researchers from population surveys that elicit individuals’ ordering of their preferences for different health states or disease conditions in any of several different ways, including responses to hypothetical time or health-state tradeoffs (Gold et al., 1996a). Developing QALY weights through survey research of this kind is a form of contingent valuation, a stated preference technique to establishing value.

Contingent valuation is “a survey-based methodology for eliciting consumers’ willingness to pay for benefits from a particular policy, usually expressed as a small change in risk” (Appendix B, p. 137). Because it directly measures the value someone places on the benefit, it most closely approximates the actual measure sought. Studies of contingent valuation can be conducted from different perspectives, such as that of a community (e.g., the average of the values given by a statistically valid population sample) or that of a single individual. The particular perspective adopted determines how the information is interpreted and should be used.

The Committee’s Approach to Valuing Health Capital

The version of health capital analysis employed here takes a comprehensive and egalitarian approach to constructing the value of life years in a particular health state by extending the value of life years beyond their potential for income production and by nominally assigning each person the same value for every year of life in perfect health. The Committee has chosen, in the analysis presented in this report, to value each year of life in perfect health at $160,000, in 2001 dollars. This is the median value ascribed to such a healthy year of life in a recent review of contingent valuation studies. The range of values from contingent valuation studies in this review extended from $59,000 to $1,176,000 per year of life (Hirth et al., 2000). Many researchers and policy makers remain reluctant to convert life years and health-related quality of life into monetary terms because they are skeptical that these very different kinds of goods, life and money, can be commensurated. Thus QALYs themselves often serve as the final unit of value (instead of dollars) for studies of the relative cost effectiveness of alternative health interventions. In her commissioned analysis, Elizabeth Richardson Vigdor uses the information about the relative health outcomes of similar people with and without health insurance that the Committee reported in Care Without Coverage and Health Insurance Is a Family Matter to estimate the value of years of life, and of quality-adjusted years of life (QALYs) that would be gained if the uninsured had coverage over the course of their lives. This analysis is summarized in Chapter 4 and presented in full as Appendix B. Additional methodological issues and choices the Committee made for this analysis are discussed in Chapter 4.

Approach to Estimating Additional Costs from Added Insurance Coverage

The increases in life expectancy and quality of life underlying the health benefits from health insurance estimated in Chapter 4 are the result of increases in health care utilization—more preventive care, more appropriate care, and improvements in access. In Chapter 5, the Committee examines the costs that would result from the additional use of health care induced by insurance. The chapter reports the results of three analyses that compare utilization and expenditures by those with and without health insurance for the full year. Because the uninsured differ from the insured in a number of characteristics that influence health and health care beyond their different insurance status, any analysis of the costs of insuring the uninsured must account for observable differences in health status, age, gender, race, education, and other factors. Each of the three studies reviewed in Chapter 5 make adjustments to account for systematic differences between insured and uninsured populations. The two more current studies also predict the cost of additional services to the uninsured under two different scenarios. The first scenario assumes that the uninsured acquire the patterns of care of those with private health insurance and the second assumes the uninsured have the patterns of care and expenditures of a similar group with public coverage.

These two benchmarks assume that what happens to the uninsured is similar to the experience of the currently insured as a group. If the scope of the benefits package, the levels of cost sharing, the provider payment, or financing of the plans for the uninsured were different from what is now typical, then the cost could differ accordingly. If there were other structural changes in the health care delivery system, then the estimates would need to be adjusted because the projections assume no shifts in the unit costs of health care services after the implementation of universal coverage.

LIMITATIONS OF THE EVALUATION OF COSTS AND BENEFITS RELATED TO COVERAGE

The Committee’s analysis in this report rests largely on the findings and conclusions related to health outcomes, family impacts, and community-level effects of uninsurance contained in its previous reports. The strengths and limitations of the evidence base for the particular findings are included in Care Without Coverage, Health Insurance Is a Family Matter, and A Shared Destiny. The estimates and discussion of costs and benefits presented in this report have additional important limitations and qualifications.

First, the Committee has quantified only some of the costs of uninsurance, and these estimates are based on a single analysis that the Committee commissioned. The Committee believes that its estimation of the health capital forgone takes a justifiedly narrow and conservative approach to quantifying societal costs and probably underestimates the value lost through uninsurance. The potential for economy-wide and employer-specific costs are discussed qualitatively, but are not quantified in monetary terms.

Second, the estimate of the value of health capital that would result from universal coverage is dependent on the value imputed to a QALY through the stated-preference technique of contingent valuation. Although the value the Committee uses is consistent with current practice in many government agencies reflecting implicit tradeoffs between money and safety, this technique and the value ascribed are both subject to development and revision with further study and application. Again, the Committee believes that the analysis presented here makes reasonably cautious and conservative assumptions.

Third, although the estimate of the direct health care costs now incurred by uninsured Americans has been derived from two independent sources and is well documented and based on reasonable assumptions (see Hadley and Holahan, 2003a), it should not be assumed that these costs necessarily would be offset or eliminated by universal coverage. The extent to which a program of universal coverage would “capture” any of these current subsidies and expenditures depends on the specific provisions of the approach adopted.

Fourth, the resource costs projected in Chapter 5 for increasing the utilization of health care services by uninsured Americans to the level of utilization by those who have coverage should not be construed as the cost of any particular program or set of policies resulting in universal health insurance coverage. Furthermore, the costs of such expansions of insurance coverage are likely to be distributed quite differently from the incidence of costs and burdens associated with the status quo. These projections answer a much narrower question than the questions that would need to be addressed in developing cost estimates for any policy reform proposal. The Committee presents these projections in order to compare the value of statistical healthy life years that would be gained by uninsured individuals if they were to acquire lifelong health insurance coverage in terms of the costs of additional services that would allow them to achieve better health.

Finally, this report and the estimates and analyses it contains are initial efforts at developing an integrated and coherent framework for evaluating a variety of economic costs attributable to the lack of health insurance across the U.S. population. It should not be the last word on the subject. Throughout the report, the Committee notes important questions that cannot be answered adequately because of the lack of data or research. Although this report does not explicitly develop an agenda for further research, the limits of what can be said about the costs due to uninsured populations implicitly point to such an agenda.

SUMMARY

This chapter has presented the analytic context, concepts, and approach that the Committee employs in the remainder of the report and acknowledged the limitations of the analysis. The following chapter considers the health care services costs incurred by uninsured Americans and identifies who ultimately bears these costs.