12

Insights on Outsourcing: The Electronic Manufacturing Services Industry for the Aerospace and Defense Markets

Charles W. Wade

Technology Forecasters, Inc.

Contract manufacturing, also known as electronic manufacturing services, gained acceptance in the mid-1980s and is now an integral part of the worldwide electronics industry. Contract manufacturing started with United States-based companies primarily supporting the computer systems and peripherals industry on a consigned material basis. Outsourcing has now expanded into a global operation, providing design, manufacturing, supply chain management, test, and order fulfillment services for the computer, telecommunications, medical, instrumentation, automotive, aerospace/defense, and consumer industries.

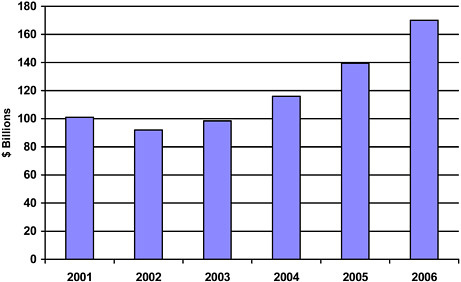

Even with the difficult economic conditions that affected the electronics business in the new millennium, the electronic manufacturing services (EMS) industry has continued its acceptance in the global marketplace. From an overall market standpoint, the worldwide EMS market is forecast to grow from $92 billion in 2002 to over $170 billion in 2006, a 16.5 percent compound annual growth rate (CAGR) (Figure 12-1).

This increase in electronic manufacturing outsourcing is a result of the positive business impact realized by original equipment manufacturers (OEMs) in the current outsourcing environment. OEMs that are outsourcing will have a competitive advantage. The expansion of outsourcing will be driven by synchronization between OEMs and EMS providers that will uncover additional cost savings and service enhancements, which will in turn drive additional benefits for the OEMs; increased competitive market cost pressures; and better management tools for the OEM/EMS relationship, which will reduce the perceived risk of outsourcing additional services.

OEM OUTSOURCING REQUIREMENTS

In studies conducted by Technology Forecasters, Inc. (TFI), several factors have been identified that OEMs want when they consider outsourcing of manufacturing. These include cost reduction and improved asset utilization; quality improvement; agility and/or flexibility; timeliness and delivery assurance; technology advancement; vertical integration leveraged from the EMS; business and/or risk management; global footprint; long-term relationships. As the leading strategic consulting firm servicing the EMS sector, TFI is in a unique position to evaluate the needs and requirements of OEMs served by the EMS providers. For 15 years, TFI has been conducting customer satisfaction interviews for EMS companies. In each interview, TFI representatives ask EMS customers qualitative and quantitative questions to measure the current level of satisfaction and ascertain the future needs of their business.

In a previous TFI study, the current needs and requirements of 72 OEMs were analyzed. The organizations surveyed included the entire spectrum of OEMs, ranging from the largest electronic firms in the world to start-up companies servicing small niche electronic markets. In

FIGURE 12-1 The global market for electronic manufacturing services. SOURCE: Technology Forecasters Quarterly Forum, December 2002.

response to questions on what constitutes EMS value and services, TFI received a total of 323 responses on items that are significant factors in choosing and maintaining a relationship with an EMS supplier. The top items in the OEM’s perception of EMS value and service are cost/price, quality, and dependable delivery.

COMMON MISTAKES IN OUTSOURCING

While consulting with over 60 OEMs on how to establish outsourcing programs, TFI identified five key outsourcing mistakes that prevent effective implementation. Table 12-1 presents these mistakes and their possible impacts.

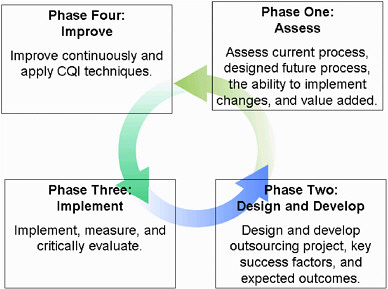

OUTSOURCING CYCLE

In consulting with clients, TFI recommends a four-phase approach to implementing the outsourcing process: assess, design, implement, and improve. Critical to the success of outsourcing is communication between all levels at the OEM and the EMS partner. Figure 12-2 illustrates this process cycle.

AEROSPACE AND DEFENSE EMS MARKET STUDY

The aerospace/defense industry is a major component of the U.S. economy, with 4,400 U.S. companies engaged in this industry in 2001, a total output of more than $200 billion and

TABLE 12-1 Common Outsourcing Mistakes and Their Potential Impacts

|

Mistakes |

Potential Impacts |

|

Incomplete, inaccurate, or late request for proposal |

|

|

Lack of consensus among OEM stakeholders |

|

|

EMS suppliers chosen casually and not strategically |

|

|

Micro-managing the EMS supplier |

|

|

Inefficient management of EMS and unclear performance expectations |

|

employment of over 3 million.1 Companies in the aerospace/defense products industry manufacture a wide range of products, including computer systems, tanks, guided missiles, aircraft, navigation systems, arms, and ammunition. These companies sell primarily to the U.S. government, although private sector markets still exist. At the request of members of the Quarterly Forum for Electronics Manufacturing, Outsourcing and Supply Chain, TFI conducted a study on EMS activity in the aerospace/defense electronics market.2

OUTSOURCING CYCLE

In consulting with clients, TFI recommends a four-phase approach to implementing the outsourcing process: assess, design, implement, and improve. Critical to the success of

|

1 |

Harris InfoSource. 2002. Aerospace/Defense Industry Report. Published at http://www.researchandmarkets.com/reportinfo.asp?cat_id=17&report_id=2891. Accessed November 2003. |

|

2 |

The Aerospace/Defense Electronics Market: Unique Hurdles and Timely Opportunities, June 2003 Quarterly Forum. |

FIGURE 12-2 The outsourcing cycle. SOURCE: Technology Forecasters, Inc.

outsourcing is communication between all levels at the OEM and the EMS partner. Figure 12-2 illustrates this process cycle.

AEROSPACE AND DEFENSE EMS MARKET STUDY

The aerospace/defense industry is a major component of the U.S. economy, with 4,400 U.S. companies engaged in this industry in 2001, a total output of more than $200 billion and employment of over 3 million.3 Companies in the aerospace/defense products industry manufacture a wide range of products, including computer systems, tanks, guided missiles, aircraft, navigation systems, arms, and ammunition. These companies sell primarily to the U.S. government, although private sector markets still exist. At the request of members of the Quarterly Forum for Electronics Manufacturing, Outsourcing and Supply Chain, TFI conducted a study on EMS activity in the aerospace/defense electronics market.4

The North American Industry Classification System (NAICS) is the U.S. government’s official system for categorizing industrial data. The aerospace/defense industry uses 14 NAICS codes, and production is spread over a wide range of activities. Products contributing heavily to total industry revenue and employment include electronic computers; communications equipment; search, detection, and navigation equipment; aircraft; and aircraft engines.

The defense industry has been a bright spot in the current U.S. economy as it has been

|

3 |

Harris InfoSource. 2002. Aerospace/Defense Industry Report. Published at http://www.researchandmarkets.com/reportinfo.asp?cat_id=17&report_id=2891. Accessed November 2003. |

|

4 |

The Aerospace/Defense Electronics Market: Unique Hurdles and Timely Opportunities, June 2003 Quarterly Forum. |

TABLE 12-2 Key Drivers and Obstacles to Outsourcing of Aerospace/Defense Electronics

|

Driver |

Obstacle |

|

Higher military budgets due to terrorism and increased tension in the Middle East and North Korea. |

Continuing slump in the travel market and financial fragility of major carriers leads to lower commercial aircraft production. |

|

Higher unit sales of replacement equipment during military build-up and hostilities. |

Security considerations and bureaucratic procedures slow shift to outsourcing. |

|

Success of high-tech military equipment in military action will lead to further development and procurement of such systems. |

|

|

Likelihood of significant military upgrading in Europe. |

|

bolstered by large budgets aimed at transforming the military for a war on terrorism and perceived foreign threats from nations such as Iraq and North Korea. This military buildup will not be able to offset the ongoing crisis in commercial aviation, however. These economic conditions will present both opportunities and challenges for aerospace/defense contractors and EMS suppliers participating in this market.

The aerospace/defense industry had faced a slump in segment growth since the mid-1990s but experienced a resurgence by the end of 2000, with increases in employment and exports. The events of September 11th, however, seem to have resulted in an almost instantaneous shift in direction for the industry. With defense contracts likely to increase substantially over the next 5 to 10 years, companies producing war-ready products and systems are likely to see an increase in revenue. Despite this defense sector growth, September 11th has negatively affected others in the industry. Nearly all airlines are losing money, tens of thousands of workers have lost their jobs, and the crisis shows no signs of improving in 2003. One casualty of the airline struggle will be orders for new aircraft. Already, surplus aircraft account for 13 percent of the world’s jetliner fleet.5 For both Boeing and Airbus, further production declines are likely. The Airline Industries Association (AIA) predicts that Boeing will cut aircraft production to about 280 aircraft in 2003, a 26 percent reduction from 2002. In January, Airbus announced plans to produce 300 jet aircraft in 2003. If Airbus meets this goal, it will surpass Boeing in aircraft deliveries for the first time.

Aerospace and Defense Outsourcing Markets

As the aerospace/defense market continues to grow, the need for EMS suppliers will also increase. TFI projects that aerospace/defense EMS revenues will grow from $4.0 billion in 2001 to $7.7 billion in 2006. This CAGR of 14.0 percent is below the EMS industry average of 16.5 percent. During this period, TFI predicts that EMS market penetration of the aerospace/defense industry (defined as the percentage of the cost of goods sold that are outsourced) will increase from 11 to 16 percent. This trend in outsourcing of aerospace/defense electronics manufacturing to EMS companies is influenced by a number of important driving forces and obstacles (Table 12-2).

Although the aerospace and defense sector represents only about 4 percent of the total

|

5 |

Business Week Online. 2003. Defense & Aerospace: Woes Not Even War Will Ease Available at http://www.businessweek.com/magazine/content/03_02/b3815714.htm. Accessed November 2003. January 13. |

EMS market, it offers some interesting possibilities for outsourcing. The electronics portion of a military system is usually a discrete black box. Therefore, the EMS company does not necessarily have to be involved in the manufacture of the larger system. In addition, military specifications, once the most stringent of design and manufacturing requirements, have now been surpassed by commercial quality standards. At most EMS companies, quality levels are sufficient to support this market due to the acceptance of IPC6 Class III standards.

Aerospace and Defense Use of Outsourcing

With the growing acceptance of electronic manufacturing outsourcing, almost all major U.S.-based aerospace/defense contractors are outsourcing to some extent. The following aerospace/defense companies currently outsource some manufacturing: Lockheed Martin; Boeing; Northrop Grumman; Raytheon; General Electric; Harris; Motorola; EADS; Rockwell Collins; United Technologies; and Honeywell.7 In a survey of aerospace/defense contractors, the following were identified as the top criteria by which they select an EMS supplier: exceptional quality; technical capability; acceptable/certified processes; financial stability; effective cost management; component management/engineering; delivery performance; and aerospace/defense experience.

When surveyed on the reasons why they would choose not to outsource or to limit their outsourcing, aerospace/defense contractors cited maintaining required quality and fear of losing control of the project as their highest concerns. Security issues, complexity of the product, concerns about an outsourcing partner’s technical capabilities, cost factors, available in-house capacity, and documentation transfer issues were also mentioned as major factors for choosing not to outsource.

EMS Participation in the Aerospace and Defense Markets

The aerospace and defense markets are attractive to EMS suppliers, and a number of service providers have strategically targeted this market segment. Table 12-3 identifies a number of EMS providers that have significant aerospace/defense business either in terms of total revenue or percentage of revenue.

When EMS companies were asked what their major challenges were to supporting aerospace/defense contractors, the most frequently mentioned factors were contract management and dealing with government regulations. This included managing documentation requirements, audits, process certification, and status reporting. Although meeting required quality standards was listed as a factor, most companies felt that their existing quality program met or exceeded the requirements for government contracts. Dealing with obsolete component issues and the issue of parts traceability indicated a strong need for component engineering and material management and control. These issues were followed by managing security requirements, lack of adequate market information, a high amount of engineering changes, low-volume, high-mix production, and required capital investment. The capital investment included specialized test equipment, conformal coating capabilities, and material management and control systems.

CONCLUSION

The global EMS market will grow to $170 billion by 2006. The aerospace/defense portion

TABLE 12-3 EMS Companies Reporting Significant Aerospace/Defense Business

|

EMS Company |

Headquarters |

Estimated 2002 Total Revenue (millions of $US) |

Estimated Aerospace/ Defense as Percentage of Total Revenue |

|

Sanmina-SCI |

San Jose, CA |

12,473 |

5 |

|

Pemstar |

Rochester, MN |

700 |

2 |

|

Suntron |

Phoenix, AZ |

300 |

2 |

|

Sparton Electronics |

Jackson, MI |

180 |

40 |

|

Sypris Electronics |

Tampa, FL |

145 |

100 |

|

LaBarge |

St. Louis, MO |

130 |

30 |

|

XeTel |

Austin, TX |

120 |

20 |

|

Metric Systems |

Ft. Walton Beach, FL |

120 |

80 |

|

SMTEK |

Thousand Oaks, CA |

80 |

10 |

|

Corlund Electronics |

Tustin, CA |

70 |

10 |

|

MTI Electronics |

Menomonee, WI |

65 |

15 |

|

Harvard Custom Mfg. |

Salisbury, MD |

60 |

35 |

|

Nortech Systems |

Wayzata, MN |

60 |

20 |

|

Teledyne Electronics |

Lewisburg, TN |

60 |

30 |

|

SMS Technologies |

San Diego, CA |

45 |

10 |

|

Raven Industries |

Sioux Falls, SD |

35 |

50 |

|

Micro Dynamics |

Eden Prairie, MN |

30 |

20 |

|

Ramp Industries |

Binghamton, NY |

25 |

20 |

|

General Technology |

Albuquerque, NM |

25 |

95 |

of the EMS market will experience moderate growth over the next 5 years. In addition to technical capability, quality and dependable delivery at a competitive price remain the primary factors for contractors when selecting and continuing to use contract manufacturing partners. Responsiveness and customer service is increasing as a critical issue in total customer satisfaction. Total supply chain and material management is one of the fastest growing areas of importance in today’s electronics market.

From the EMS perspective, finding effective ways to navigate the requirements and regulations of government contracting is essential to participation in the aerospace/defense market. Also, providers must adhere to the industry’s quality standards. The need for an effective material control system and component engineering capabilities to support this market will be critical.

Clear communication between aerospace/defense contractors, EMS suppliers, and other members of the supply chain concerning needs and requirements is critical for the survival of all. Only through open and honest dialogue can each stakeholder gain the benefit of understanding the technical and business issues facing each group in the current global electronics market.