6

A Path Forward

The previous chapters established several important results. First, rapid improvements in digital imaging and reprographic technologies are bringing professional-class capabilities to opportunist and petty criminal counterfeiters. Second, the Internet is affording all classes of counterfeiters improved means of “sharing best practices” and sourcing specialty materials (for example, substrates, color-shifting inks) so that the quality of counterfeits is improving rapidly. The implications of these trends are that the pace of the design cycle of new Federal Reserve notes (FRNs) must be sped up and that new counterfeit-resistant features must be incorporated quickly. The third important result established in this report is that there is an ample supply of concepts for such new features. Potential intermediate-term features (available within 7 years) are described in detail in Appendix C and discussed in Chapter 4. Radical new ideas for fundamentally changing the platform for currency are presented in detail in Appendix D and discussed in Chapter 5. Taken together, these results establish that even though the counterfeiting threat is growing more rapidly, potential means of countering this threat lie on the horizon.

This situation poses a challenge for the Bureau of Engraving and Printing (BEP), however. Faced with the enhanced counterfeiting threats, it will need to respond in new ways to counter them. Over the short term, the bureau will need to find a way to sort through the myriad of possibilities for new features in order to select and to implement those it believes to be most able to counter the threats. Over the longer term, it could establish research partnerships, probably with other federal agencies, to examine fundamental changes to its currency platform. This final chapter applies

some of the learning from aerospace product-delivery processes and government acquisition processes to the problem of developing and sourcing these new features and feature platforms by the BEP. While not intended to be comprehensive, this chapter is designed to highlight the magnitude and scope of these tasks in order to indicate at a high level what is involved in accomplishing them.

TECHNOLOGY TRENDS

Advanced features, described in Chapters 4 and 5, cover a wide range of technologies. Anticounterfeiting features on banknotes have in the past been primarily intended as observable features—that is, visible features produced by two-dimensional printing technology. Innovative features rely on a broad set of technologies that can significantly raise the counterfeit-deterrent bar but also require expertise in a range of materials science and engineering disciplines, as demonstrated by Table 6-1, which summarizes the different physical technologies used in the features presented in Chapters 4 and 5. Most of these features apply two or more of these technologies. Today’s visible features, by comparison, primarily employ a single physical technology.

The trend in increasing technological complexity is illustrated in Figure 6-1. This figure notionally depicts the temporal evolution of the features that are currently in use and those described in this report. Those new features, discussed in Chapter 4, that can be readily developed for implementation within the next 3 to 4 years employ feature technologies and production methods similar to those used for the current features, even though the new features would be more difficult to simulate and more recognizable. However, the features beyond this generation of innovations will exploit advanced technologies that extend into the composite and active-feature realm and necessarily require new manufacturing processes, such as microfabrication.

The ultimate goal is to move feature technology beyond the capabilities of digital reprographic technology and thereby significantly reduce threats posed by

TABLE 6-1 Technologies Employed in the Innovative Features Described in This Report

|

Technology Category |

Features Using This Technology (no.) |

|

Chemistry |

9 |

|

Computing |

4 |

|

Electronics |

8 |

|

Materials |

11 |

|

Mechanics |

6 |

|

Optics |

16 |

|

Sensors |

9 |

FIGURE 6-1 A notional depiction of the evolution of human-detectable features in currency. This chart shows features that are now in use in U.S. currency and those proposed in this report, as a function of feature technology (left axis)—that is, active, composite, substrate, and print; and as a function of the manufacturing technology (right axis)—that is, microfabrication, special materials, and conventional printing—required to produce the feature. This chart is a schematic that has been drawn to give a general idea of how currency features—and in particular human-detectable features—have evolved and will evolve in the future in relation to technology. NOTE: Near-term features: 3 to 4 years for implementation; intermediate features: within 7 years for implementation; disruptive feature platforms: more than 7 years for implementation.

the opportunist and the petty criminal counterfeiter. The grand challenge is to accomplish this new level of deterrence while maintaining the distinctive character of the U.S. Federal Reserve note and producing these advanced notes at an affordable cost to the Federal Reserve System. This grand challenge is the crux of the research strategy that the committee is hypothesizing for each of the innovative features. The major aspects of this strategy are indicated in the following sections.

FEATURE-DELIVERY PROCESS

The development of innovative counterfeit-deterrent features such as those proposed in this report all the way from the research and development (R&D) stage to implementation in FRNs presents a number of challenges. Not only does the development program of a feature have to meet its expected technical outcome, but also the use of the feature needs to (1) maintain the traditional “look and feel” of U.S. FRNs, (2) allow the FRNs to perform suitably in the appropriate qualification wear-and-tear tests, (3) be compatible with the banknote production process, (4) maintain the effectiveness of the feature over the lifetime of the banknote, and (5) not pose any hazard or use restrictions to the public.

Many of the innovative feature ideas presented in this report leverage work in fields outside of security printing. This work can provide a considerable benefit in accelerating the work required for a full understanding of the physical phenomena that form the basis for the deterrent, as well as providing the technical support for investigating the proof-of-concept.

The considerations highlighted above suggest that a formal phase-gate feature-delivery process is required to create the needed features on budget in a timely fashion. Thus, the committee adapted existing technology- and product-delivery processes in order to propose a four-phase feature-delivery process that could be used by the BEP to convert feature suggestions such as those articulated earlier in this report into delivered new features on FRNs.

Where applicable, references are provided for the features listed to relate what is available in the literature regarding the science and technology to a particular feature or feature platform. Those feature technologies that are well explored have a relatively extensive reference set. There are two additional considerations. The first is that the basic physics of the feature should be obvious. For example, in the case of using grazing-incidence illumination for surface deformations in the currency substrate (the basis for the grazing-incidence optical patterns feature proposed herein), diffraction is the operative physical effect. The idea may be new for currency, but optical science books would adequately describe the physical phenomena.1 Additional references would not add value in such a case. Second,

some features may be so new as not to have available references. The major risks of the feature and feature platforms cited in this report are not the fact that their functional capabilities have to be proven, but rather that what has to be proven is that their application in the production of U.S. currency is useful in deterring counterfeiting, that they can be implemented cost-effectively, and that they provide the expected durability and distinctive appearance of the FRN.

Feature-Delivery Phases

The committee regarded the delivery of a new counterfeit-deterrent feature as comprising four phases, which are adapted from NASA’s Technology Readiness Levels2 and the Department of Defense’s Manufacturing Readiness Levels.3 Phase 0 begins the process with idea generation, a thorough literature review, the identification of related work, and an outline of a plan for Phase I. Phase 0 concludes with a specific list of what should be demonstrated in order to make the feature a viable candidate for insertion in a banknote. Phase I focuses on obtaining proof-of-concept for the new feature idea. During this phase, proof-of-concept analyses and experiments are conducted, and application scenarios are developed. During Phase II, feature attributes are developed, along with the requisite manufacturing technology, so that the feature can meet the requirements for a targeted banknote application. Phase III begins with a decision to incorporate the new feature in a specific banknote. At the completion of Phase III, the feature is ready for full production in a banknote.

At the conclusion of each of these phases, a decision would be made to terminate or to continue the development of the feature into the next phase. Of course, the R&D effort can be halted during any phase if the results or projected benefits are not attractive enough for eventual implementation. A description of the four individual phases is summarized in Boxes 6-1 through 6-4:

-

Phase 0: Idea Generation and Scoping (Box 6-1),

-

Phase I: Establishment of Feasibility (Box 6-2),

-

Phase II: Demonstration of Applicability (Box 6-3), and

-

Phase III: Maturation and Scale-Up (Box 6-4).

|

2 |

The definition of Technology Readiness Levels is available at the Web site of the National Aeronautics and Space Administration (NASA) at <http://esto.nasa.gov/files/TRL_definitions.pdf>. Accessed February 2007. |

|

3 |

The definition of Manufacturing Readiness Levels is available at the Web site of the Defense Acquisition University at <https://acc.dau.mil/CommunityBrowser.aspx?id=18231>. Accessed February 2007. |

|

BOX 6-1 Phase 0: Idea Generation and Scoping Objective: Provide specificity to a counterfeit-deterrent feature idea. Accomplishing this will require the following:

|

|

BOX 6-2 Phase I: Establishment of Feasibility Objectives: (1) Demonstrate the feasibility of a new feature and (2) identify credible application scenarios. Reaching these objectives would require the following:

|

|

BOX 6-3 Phase II: Demonstration of Applicability Objectives: (1) Identify a specific targeted application that would significantly benefit from the new feature and (2) obtain sufficient data to characterize the risks, costs, and benefits so that an “application go-ahead” decision can be made. Reaching these objectives would require the following:

|

Some features could be expressly designed for detection by commercially available currency-reading equipment. Currently the BEP does not provide banknote feature specifications to commercial equipment manufacturers. Registered vendors have an opportunity to examine “test decks” containing relevant features prior to the issuance of a new series note. They use these decks to determine which feature(s) to select for detection and what technical approach to employ. The resulting equipment is then marketed to vending-machine suppliers, retail stores, commercial banks, and so on. For the future, as machine reading becomes more pervasive and the feature technology more sophisticated, the government may consider a proactive approach in providing these registered vendors with test decks earlier, possibly during Phase II of the development program. This approach would allow the vendors more time to develop and optimize their detection technologies for the new features. This capability would provide a useful benefit to the public

|

BOX 6-4 Phase III: Maturation and Scale-Up Objectives: (1) Incorporate the new feature into the design of a specific banknote series, (2) qualify the new feature, and (3) complete efforts necessary to scale up the feature production and incorporate it into the banknote. Achieving these objectives requires the following:

|

and commercial cash handlers who expect machine readers to work effectively with new series notes, as well as with the older series notes. Necessary precautions would have to be taken to ensure that the earlier consultation process with vendors did not threaten the security of new features.

Development Risk and Issues

For each feature discussed in Chapter 4, the committee identified a list of significant risks and issues that should be addressed during a development program for that feature. These risks and issues (presented in Appendix C) include an understanding of the feature’s inherent durability limits; appearance and aesthetic considerations; issues related to social acceptability, such as potential health hazard concerns and loss of privacy—for example, the ability to scan a person and determine the amount of cash being carried; and key technical challenges.

Table 6-2 summarizes the key technical challenges, abstracted from Appendix C, for each feature described in Chapter 4. Similarly, Table 6-3 summarizes the

TABLE 6-2 Key Technical Challenges for Intermediate-Term Innovative Feature Concepts Described in Appendix C

|

Innovative Feature Concept |

Key Technical Challenges |

|

Color image saturation |

|

|

Fiber-infused substrate |

|

|

Fresnel lens for microprinting self-authentication |

|

|

Grazing-incidence optical patterns |

|

|

High-complexity spatial patterns |

|

|

Hybrid diffractive optically variable devices |

|

|

Metameric ink patterns |

|

|

Microperforated substrate |

|

|

Nanocrystal pigments |

|

|

Nanoprint |

|

|

Refractive microoptic arrays |

|

|

See-through registration feature |

|

|

Innovative Feature Concept |

Key Technical Challenges |

|

Subwavelength optical devices |

|

|

Tactile variant substrate |

|

|

Thermoresponsive optically variable devices |

|

|

Window |

|

key technical challenges, abstracted from Appendix D, for each feature described in Chapter 5. The committee envisions that these challenges would be refined during Phase 0 and would become the focus of development activity during Phase I in order to establish the feasibility of the feature concept.

The committee suggests that every feature idea, regardless of the amount of related prior work, begin development with a Phase 0 task. This would establish a firm baseline for the development effort. For features that employ the more mature technologies, Phase 0 could be relatively short. Similarly, the effort to demonstrate proof-of-concept during Phase I may not be large for these features. It is critical though that feasibility be demonstrated against banknote design requirements before proceeding to Phase II. By contrast, immature feature concepts could require considerable effort in Phases 0 and I.

As one might expect, a good anticounterfeiting feature should be aesthetically pleasing, since currency is not just functional but also a form of national identity that is especially recognizable. Thus, the features suggested in this report have been examined with respect to their effect on the FRN’s overall aesthetics. Clearly, aesthetic design is difficult to quantify, but any new features should not adversely impact the look and feel of the currency. For many of the features proposed in this report, gauging the aesthetic impact will not be possible during Phase I because the final form of the feature has not yet been determined. However, the committee considered what potential impact a proposed feature could have on the look, feel, and overall appearance of an FRN. Concerns regarding the aesthetics of a particular feature are listed under challenges and should be evaluated along with the other challenges.

Table 6-4 summarizes the key milestones that should be achieved during Phase I for the features discussed in Chapter 4. Specific milestones for Phases II

|

Innovative Feature Concept |

Key Technical Challenges |

|

Smart nanomaterials |

|

|

Tactilely active electronic features |

|

and III, beyond what is described above in general, depend to a large extent on the results of Phase I. As previously mentioned, some of the innovative features in Table 6-4 will proceed through Phase I rather quickly owing to their simplicity, the extent of related development work, or their potential to serve as a direct replacement for an existing feature. Other features will take considerably longer for a demonstration of proof-of-concept and feasibility.

All of the long-term feature platforms summarized in Table 6-3 will require considerable time for development. The primary Phase 0 milestone for these features would be a roadmap for the most promising development routes. One strategy for development of these long-term concepts is to maintain a long-term core development effort in Phase I. As the Phase I work proceeds, specific feature ideas would be identified for a targeted application. In this case, a new project would be started in Phase I for the feature idea that was spun out of the more general development program for the feature platform with the intent of proceeding on to Phases II and III as the technology is matured. For example, the e-substrate is not a feature itself but an enabler for other active features. The Phase I effort would maintain awareness of related developments and would conduct feasibility assessments of the most promising approaches. If an active feature were identified as a high priority, the appropriate elements of the e-substrate would be incorporated into the active-feature development program as it progressed from Phase I into Phases II and III. By contrast, a specific feature idea, such as engineered cotton fibers, could proceed through the development phases once feasibility was established in Phase I.

Single Feature Versus a Set of Features

The committee acknowledges one key limitation of this report: the innovative features and concepts were evaluated by considering the effectiveness of each fea-

TABLE 6-4 Summary of Phase I Milestones and Timing for Intermediate-Term Innovative Feature Concepts Described in Appendix C

|

Innovative Feature Concept |

Key Milestones—Phase I |

Estimated Time to Complete Phase I |

|

Color image saturation |

|

● |

|

Fiber-infused substrate |

|

●● |

|

Frensel lens for microprinting self-authentication |

|

●● |

|

Grazing-incidence optical patterns |

|

● |

|

High-complexity spatial patterns |

|

● |

|

Hybrid diffractive optically variable devices |

|

●● |

|

Metameric ink patterns |

|

● |

|

Innovative Feature Concept |

Key Milestones—Phase I |

Estimated Time to Complete Phase I |

|

Microperforated substrate |

|

● |

|

Nanocrystal pigments |

|

●● |

|

Nanoprint |

|

●● |

|

Refractive microoptic arrays |

|

●● |

|

See-through registration feature |

|

● |

|

Subwavelength optical devices |

|

●●● |

ture independent of all other features that might be present in a singe banknote. To the degree that the committee has studied the interaction of features, it can, however, conclude the following:

-

Many features are not truly independent—they can complement, or in some cases degrade or even negate, the effectiveness of other features.

-

Reliance on a single dominant feature can provide false security if that feature can be replicated well enough and users do not inspect other features. Prominent features can create a focus of attention that negates others, so that the counterfeiter can replicate or simulate the dominant feature and ignore other security measures. For instance, color is a dominant feature. But current reprographic technology can easily replicate the appearance of the color note, thereby decreasing the chance that a consumer would check other features. Thus, avoiding over-reliance on a dominant feature should be included in the evaluation process for selecting features; this consideration would also apply to machine-readable features.

-

To the degree that several new features may be more effective than a single feature, they should be incorporated as a set of features so as to provide

-

a layered defense against an array of counterfeiting threats. Such an approach will create a public awareness of multiple features on the note and reduce the reliance on a single dominant feature. Multiple features can also address the various classes of counterfeit threats; for example, color image saturation and metameric ink features would target nonprofessional counterfeiters, while the fiber-infused substrate and the nanoprint features would target professional counterfeiters.

BANKNOTE DESIGN PROCESS

The feature ideas that originated during the course of this study arose out of a technology-push perspective—that is, the committee considered what could be possible and then used various criteria to refine the list. This report necessarily does not contain an exhaustive list of all possible new features. Additional technologies undoubtedly could be successfully employed to improve counterfeit deterrence. However, the committee believes that the process followed in conducting this study would be applicable to the analysis and development of other candidate features. Ultimately, in order to be useful, an innovative technology must be proven effective. The goal is to provide banknote designers with new counterfeit-deterrence feature options that they can employ to stay a step or two ahead of the advancing counterfeit technology. These options will allow the designers to engage in assessing the “art of the possible” as they (1) synthesize the totality of needs and requirements that a new banknote must satisfy, (2) analyze the functions that the new banknote must perform in order to meet those requirements, and (3) determine how best to allocate requirements to the various components and features that comprise the banknote. The collection of these activities required to design new features and incorporate them into banknotes is the banknote design process.

This proactive approach differs significantly from the traditional approach, which entails an evaluation of mature counterfeit-deterrence features for which most of the issues have already been addressed, for which a supply chain exists, and which are already in use with known effectiveness.

For the proactive approach, candidate innovative features would proceed through the development phases with an increasing focus on a targeted banknote application. Therefore, the advocacy for feature development must transition to a technology-pull mode in which the banknote designer has a significant role. The successful features will survive trade-offs between competing factors with respect to the banknote’s production cost, implementation schedule, and technical performance. Also, during the phased development process, some of the innovative features will be found to be noncontenders for insertion. The reasons would include shortfalls in performance that cannot readily be overcome, a high production cost that is not amenable to cost reduction during scale-up, excessive time to complete

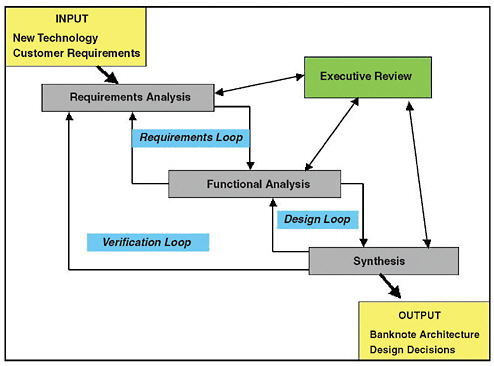

FIGURE 6-2 Design engineering process. SOURCE: Adapted from John B. Wissler, 2006, Technology transition: A more complete picture, Defense Acquisition Review Journal 13(1):10 (Fort Belvoir, Va.: Defense Acquisition University Press).

development because of the large number of complex issues that must be addressed, and the ready availability of another feature that can better satisfy almost all of the key requirements.

The design engineering process is necessarily an iterative one, as depicted in Figure 6-2. It is through this mechanism that the transition from the technology-push to the technology-pull development focus occurs. The design process is overseen by an executive review that allocates resources, establishes time lines, conducts trade-offs between suites of features, and makes “go/no-go” decisions on the continuation of a particular project. As illustrated in the figure, the key starting point of the design engineering process is the input of new technology that occurs during Phase 0. Requirements definition is one of the primary activities initiated during Phase I. Through this mechanism, a banknote designer can establish the requirements for a feature and then evaluate the proof-of-concept results against these requirements. As the development proceeds through the subsequent phases, these requirements will be refined and developed in more detail until they are finalized

during Phase III, as indicated by the Requirements Loop. Design of a feature is also an iterative process. It is formally initiated during Phase II when the prospective feature is targeted for a specific application. This serves as the basis for identifying needed information, so that the effort expended during Phase II is focused on collecting the data to support these information needs. Further data will be collected during Phase III to support the production go-ahead decision as functional analysis and synthesis of design solutions are accomplished. Finally, verification tests the design solution against the latest requirements. This is a key activity as Phase III proceeds. If the design solution falls short of requirements, further review of the requirements and the design solution would be necessary, as depicted by the Verification Loop. When Phase III is successfully completed, the new feature will be incorporated into the banknote architecture, ready for production.

PROGRAM-EXECUTION CONSIDERATIONS

Many more feature ideas are presented in this report than can be funded for development. The committee was unable to further prioritize the features beyond selecting the most promising ones for listing in the report. The experts at the BEP could use the information in this report as the basis for further prioritization, thereby determining which features have the most promise for addressing gaps in deterrence beyond what is already planned. It would be important to consider the long-term as well as shorter-term needs to establish a balanced portfolio of features for development.

Some of the feature ideas in this report could readily be explored by the BEP working with equipment and other suppliers. Other feature concepts will require considerable expertise in technology areas for which the BEP has had little, if any, experience. In these cases, partnering with another federal agency that already has relevant expertise could allow the BEP to make rapid progress without incurring large expense if it is the intent of the bureau to own the intellectual property rights of the new feature(s). At some point in the development program, such as during Phase II, the supporting supply chain would be incorporated into the program.

The committee has identified a number of new ideas that require further exploration, and other ideas can be added. These ideas are extremely broad ranging, from an idea that could readily proceed through the development stages in a few years (for example, a see-through registration feature) to game-changing concepts that require significant development over multiple years, perhaps a decade (for example, smart nanomaterials).

Although it is outside the committee’s charter to recommend a particular scope for such a research program, the magnitude of the task of evaluating the concepts articulated in Appendixes C and D suggests the need for a two-pronged approach. For the intermediate-term innovative features, the essence of the task is to select the

most promising features for immediate implementation. The BEP could perform this task internally. Although suppliers can help with certain details, the research to evaluate and to select certain features above others could be done internally.

For the longer-term, disruptive platforms, partnerships with other federal agencies seem to be an attractive option. In this case, the BEP would work with other agencies to get its objectives embedded into long-term joint research programs on advanced technology (for example, nanotechnology). The currency experts at the BEP would review the results of these programs jointly with the primary sponsoring agencies on a regular basis to ensure that its needs are being addressed adequately. By analogy with comparable government and industry efforts, the committee believes that a significant multimillion-dollar annual budget would be required to provide seed funding for Phase 0 and Phase I projects, with the amount determined by BEP requirements. A program of this scale would allow a balanced program of low-risk and high-risk, game-changing technologies to be pursued. This could build a portfolio of counterfeit-resistant features addressing short-term, intermediate-term, and long-term threats. Once plans were solidified and priorities established in Phase I, appropriate funding for Phase II and Phase III efforts could be established.

FIELD TESTING OF FEATURES

During the course of this study, the committee observed that there does not appear to be a scientifically based federal program dedicated to field testing the effectiveness of existing and proposed banknote features and feature sets. It is normal commercial practice to conduct thorough market tests of new products. The committee was made aware of only two studies of the effectiveness of some features used on older series notes.4,5 These laboratory-based experiments presented suggestions concerning the various factors that might influence the “passing effectiveness” of a note, but they do not produce the quantitative information needed to estimate the chance that a particular banknote feature combination would be successfully passed in an actual, real-world transaction.

Several major banks and commercial currency manufacturers have active programs that study feature effectiveness and pursue research on new technologies to deter counterfeiting. These efforts often supplement aggressive public awareness campaigns by a central bank to introduce new security features in banknotes. Also,

the committee noted that the Bank of Canada—the Canadian central bank and equivalent of the Federal Reserve—conducts research in the visual and optical evaluation of banknote features, including user studies to test the ability of professionals and nonprofessionals to detect counterfeit notes. The National Printing Bureau of Japan, which prints Japanese currency, includes on its staff expertise in image processing and optics, and its researchers regularly publish in conferences related to digital imaging and counterfeit technology. De La Rue International (with Portals Bathford), a private company that prints currency for a multiplicity of countries, employs expertise in image processing and optics in its feature planning and production. Many international currency-related organizations employ, on a continuing basis, teams of experts similar to the committee that produced this report, and their research extends to the sponsorship of collaborative research with industry and academia partners.

The BEP could pursue a similar, ongoing research activity to conduct formal, statistically valid field tests to determine the effectiveness of features, materials, and technologies in banknote currency. Currently, the U.S. Secret Service collects data on counterfeit usage domestically and abroad, and the BEP has several effective measures to test the durability of banknotes. These efforts effectively monitor counterfeit use and sustainability. They are not designed to address the effectiveness and social acceptability of security features. Research that evaluates the visual, tactile, and aesthetic acceptance of banknote features and the ability of the different types of human cash handlers to use these features to detect counterfeit notes could provide valuable insight into future banknote design.

CONCLUSIONS

-

Rapid advances in digital imaging and reprographic technologies have created enhanced threats of counterfeiting which, in turn, could compel the Bureau of Engraving and Printing to respond in new ways to the evolving threat.

-

A proactive strategy of incorporating counterfeit-deterrent features that are a step or two ahead of the technology available to counterfeiters requires that government efforts be directed at feature innovation rather than focused only on feature integration.

-

The committee has identified a list of innovative features that have a high potential to deter counterfeiting, particularly by opportunist and petty criminal counterfeiters. In general, these features employ technologies that are not being developed for currency applications and will not advance to a stage at which they can be readily incorporated into Federal Reserve notes without dedicated research and development for application.

-

In the future, as machine reading becomes more pervasive and banknote feature technology more sophisticated, the government may consider a proactive approach in working with equipment and other suppliers during the development of new features. This would benefit the public that expects machine readers to work effectively with new series and older series notes.

-

There is a clear need for sustained research and development of banknote features, materials, and technology. The innovative feature ideas presented in this report require R&D funding to establish feasibility for application in U.S. banknotes and to make them ready for production implementation. By analogy with comparable government and industry efforts, the committee believes that a significant, multimillion-dollar annual budget would be required to provide seed funding for Phase 0 and Phase I projects of low-and high-risk technologies, with the amount of funding determined by BEP requirements.