3

Changing Patterns of Health Insurance and Health-Care Delivery

This chapter describes recent changes in the structure of health insurance and health-care delivery in the United States and how the changes have altered how people who have chronic diseases and disabling conditions receive health care. Over the past several decades, there have been many efforts to change incentive structures in health care, all with the goal of reducing health-care costs while improving patient health outcomes. Most important among them was the Patient Protection and Affordable Care Act (ACA), which was signed into law on March 23, 2010. The ACA was the largest federal health policy initiative since the creation of Medicare and Medicaid. It brought about structural changes in the health-care system, which included efforts to improve access to health-care insurance (through expansion of the Medicaid program and through subsidized and lower-cost health insurance plans made available through new health insurance marketplaces, or exchanges), elimination of pre-existing condition restrictions in coverage, elimination of lifetime caps on health-care spending, and slowing of growth in healthcare costs through innovative payment reforms.

Although the details differ, most reforms brought about by the ACA and other efforts in recent decades have sought to reduce costs and improve patient health by expanding access to care, introducing management and coordination of care, improving quality of care, shifting risk from insurers to providers and patients, and shifting care provision from costly settings—such as hospitals, emergency departments (EDs), and long-term care facilities—to less expensive outpatient, office, community, and home settings. High-cost, high-need people have been a focus of most reform efforts because they have the greatest need and thus account for a disproportionate share of health-care spending.

The ways in which people who have chronic diseases and disabling conditions receive health care have changed in fundamental ways in terms of the kind of care they receive, how much care they receive, which providers administer the care, in which settings they receive care, and even the time of day at which they receive care, for example, during the workday or after work.

In the sections that follow, the committee begins with an overview of health insurance in the United States and of the many changes brought about by the ACA. That is followed by a discussion of the health-care delivery system, which explains how delivery system reforms brought about by the ACA and other efforts have altered the structure of health-care delivery. The committee concludes by summarizing the research evidence on how the utilization patterns

and health outcomes of people who have chronic diseases and disabling conditions have evolved in response to those changes.

HEALTH INSURANCE IN THE UNITED STATES

Health care in the United States is financed by a combination of public and private insurance, employers, and individuals who pay out of pocket. In 2015, 37 percent of the US population received health care through a public insurance program at some time (USCB, 2016). The major public insurance systems are Medicare and Medicaid. Medicare is a national health insurance program for people over 65 years old, people who have end-stage renal disease or amyotrophic lateral sclerosis, and people who have long-term disabilities once they have qualified for Social Security Disability Insurance (SSDI). It is paid for through a combination of Medicare payroll tax revenues, federal tax revenues, and beneficiary premium payments (and a small amount of state funding for the Medicare Part D prescription-drug benefit). In 2016, Medicare benefit payments totaled $675 billion and accounted for 15 percent of the federal budget, according to a report by the Kaiser Family Foundation (2017a).

Medicaid is a means-tested public insurance program that is jointly funded by the federal and state governments, but is administered by the states. Before the ACA, Medicaid covered people who were categorically eligible for benefits on the basis of income and other requirements determined at the state level. Eligibility categories include low-income children and their families, low-income people who are 65 and older, and low-income adults and children who have disabilities. Some states voluntarily extended Medicaid to other eligibility categories, such as people who have high medical expenses and the long-term unemployed. Total Medicaid spending was $574.2 billion in the federal fiscal year (FY) 2016 (KFF, 2016a).

According to a report by the Kaiser Family Foundation (2015a), Medicaid is the major insurer, public or private, that provides comprehensive coverage for institutional and community-based long-term services and supports (LTSS), which is arguably the most important form of service for people who have disabilities and need assistance with daily self-care tasks. Since the Supreme Court’s Olmstead decision in 1999, Medicaid has shifted from providing LTSS to people who have disabilities in institutional settings, such as hospitals and long-term care facilities, toward providing LTSS in home and community settings (KFF, 2015a). Although Supplemental Security Income (SSI) qualification grants categorical eligibility for Medicaid, people who are not enrolled or who might be applying for SSI or SSDI but who need long-term services and supports can obtain Medicaid coverage if their income and assets are below designated thresholds. In some states, people who have somewhat higher incomes can qualify if they meet disability-related functional criteria and, in some cases, pay a monthly “buy-in” premium (KFF, 2015a). The ability to buy into Medicaid is critical for many low-income people who have disabilities and require self-care assistance in the home or community setting in order to work; private insurance plans, including employer-sponsored plans, do not provide complete coverage of LTSS. The ACA, by expanding access to Medicaid coverage, extended that benefit to more people who have disabilities. Medicaid spending for institutional and community-based LTSS totaled more than $123 billion in 2013 and accounted for 28 percent of total Medicaid service expenditures in that year and 51 percent of total national spending on LTSS (KFF, 2015a). In addition, the federal government provides funding to federally qualified health centers whose mission is to provide direct medical services to the uninsured.

Other public insurance systems include more targeted programs, such as the Children’s Health Insurance Program (CHIP), a means-tested health insurance program for uninsured children in low-income families (administered through Medicaid in some states but as a separate program in others); the Indian Health Service (IHS)1; the US Department of Defense (DOD) health-care system (which provides health care for active-duty and retired US military); the DOD disability system (which provides SSDI benefits for injuries sustained during military service); and the US Department of Veterans Affairs (VA) health system, which provides medical care to veterans, many of whom qualify for disability benefits through VA and through SSDI or SSI.2

Private health insurance is the most common form of health insurance in the United States: 67.2 percent of the population had private coverage at some point during 2015 (USCB, 2016). Private health insurance continues to be predominantly employer based. In 2015, 55.7 percent had coverage through an employer, and 16.3 percent purchased private individual coverage directly from an insurer (USCB, 2016).3 Employers offer health insurance as a tax-advantaged benefit to employees, paying a portion of the premium for employees and their dependents. Although the employer share of health insurance premiums is considered an expense for employers like other forms of compensation, employer contributions are tax-free to employees, and employees can pay for their share of health insurance premiums on a pretax basis through payroll deductions. Before the ACA, dependent children could remain on their parents’ insurance policies through the age of 18 years or until completion of a college education, but they could have a gap in insurance coverage if they did not start jobs before the coverage lapsed. After the ACA, dependents could remain on their parents’ policies through the age of 26 years.

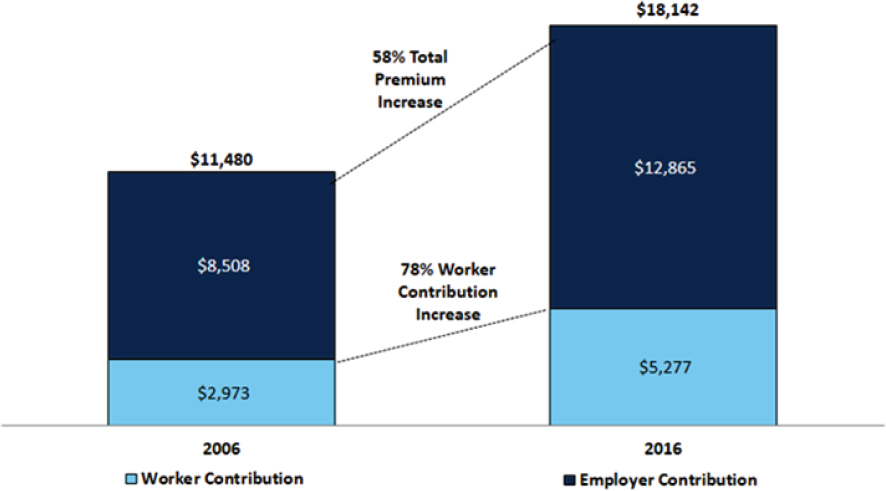

As health-care costs have risen in recent decades, employers have asked employees to share increasingly in the cost of their health care. Employees now pay a higher share of premium costs and face higher coinsurance, copayments, and deductibles than a decade ago (see Figure 3-1). For instance, while the average premium has increased by 58 percent since 2006, the average employee contribution to the premium has increased by 77 percent (KFF, 2016b).

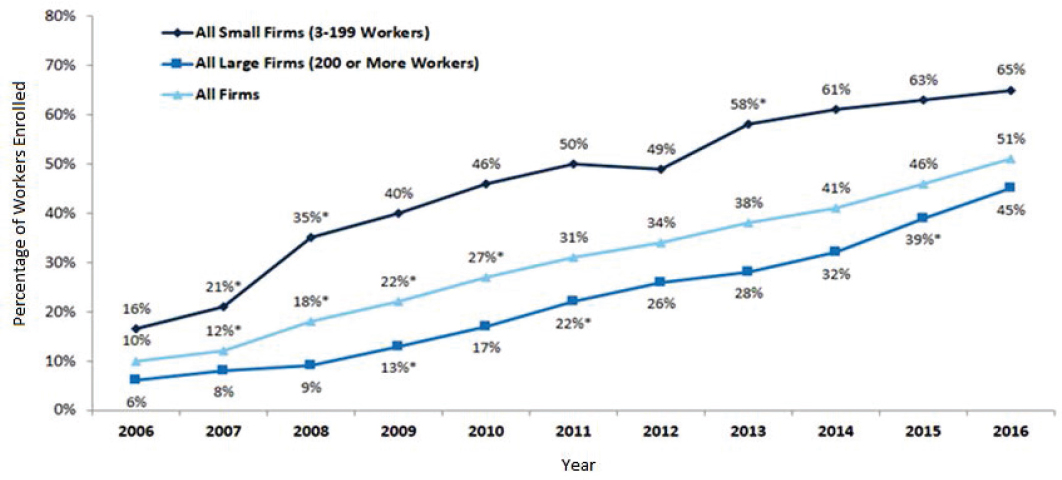

Moreover, employees are increasingly likely to face greater cost-sharing in the form of high deductibles (see Figure 3-2). About 29 percent of people who have employer-sponsored health insurance are enrolled in a high-deductible health plan (HDHP) (KFF, 2016b). By not providing first-dollar coverage for health-care services, HDHPs create strong incentives for people to reduce consumption of health-care services. People enrolled in HDHPs with deductibles of at least $1,300 for one person ($2,600 for a family plan) can save for medical expenses on a pretax basis in health savings accounts (HSAs). If not spent during a calendar year, HSA savings roll over to the next year with interest. Some employers offer HSAs as an employment benefit. Although HDHPs are intended to reduce low-value care and encourage selection of lower-priced providers, recent evidence shows that they result in reductions not only in low-value care but in potentially high-value care (Brot-Goldberg et al., 2017).

___________________

1 IHS, an agency in the US Department of Health and Human Services, is responsible for providing federal health services to American Indians and Alaska Natives.

2 Adjusted for inflation to 2014 dollars, VA disability compensation of veterans amounted to $54 billion in 2013 (CBO, 2014).

3 Coverage categories are not mutually exclusive; some people switch coverage during a year or have multiple forms of coverage.

SOURCE: KFF, 2016b.

NOTES: *Significantly different from estimate for the previous year shown (p <0.05). These estimates include workers enrolled in HDHP/SO (high-deductible health plan with savings option) and other plan types. Average general annual health plan deductibles for PPOs (preferred provider organization), POS (point-of-service) plans, and HDHP/SOs are for in-network services.

SOURCE: KFF, 2016b.

Smaller employers purchase health insurance for their employees through the small-group market, which is more expensive than health insurance sold through the large-group market because small employers have fewer employees among whom to spread the health-expenditure risk. The smaller populations in these plans make them more vulnerable to adverse selection—the tendency for those with higher expected health-care expenditures both to sign up for health insurance and to select plans that have more generous coverage. The same is true of the individual market, in which people can purchase private insurance directly from some insurers. Before the ACA, individual insurance plans were considered to pose a high risk to insurers because people who had higher expected utilization were more likely to sign up for health insurance, and this would result in severe adverse selection. When that occurred, insurers raised premiums to cover the higher claims costs, which in turn caused healthier people to leave the plans. That cycle repeated until only high-cost participants remained and the plans terminated.

The risk of adverse selection motivates many structural features of private health insurance that are designed to ensure that health plans have large risk pools with sufficient healthy, low-cost participants. In the individual market, insurance companies would protect themselves financially by using medical underwriting (charging higher premiums for those who have chronic conditions) and by precluding benefits for pre-existing medical conditions for a fixed period. Adverse selection is also why most states have created high-risk pools as a way of guaranteeing that the sickest, highest-cost people, who would otherwise be uninsurable, have access to health insurance coverage. High-risk insurance plans have higher premiums than regular insurance plans, but premiums are regulated and subject to caps (KFF, 2016c).

In 2009, the year before passage of the ACA, about 52 million people, or 15 percent of the US population, lacked health insurance. This included low-income people who did not meet Medicaid income limits or categorical eligibility and working people, usually those who were self-employed or working for a business that did not offer health insurance as a benefit. But lack of insurance did not necessarily mean total lack of medical care, owing to the Emergency Medical Treatment and Labor Act (EMTALA) and access to federally qualified health centers. EMTALA ensures that EDs provide patients with emergency care regardless of their insurance status or ability to pay (CMS, 2012). EMTALA guarantees universal emergency care access for all Americans, but it is an unfunded mandate that is partially addressed through Medicaid disproportionate share hospital (DSH) payments.4 Hospitals bear the burden of providing not only uncompensated emergency care to patients but nonurgent services inasmuch as many of the uninsured use EDs for all their health-care needs, knowing they will not be turned away (American College of Emergency Physicians, 2016). EMTALA ensures access to care for the uninsured, but ED visits are expensive and tend to result in people flowing back into the hospital for reasons that could have been avoided with adequate primary and specialty care.

A major goal of the ACA was to extend health insurance coverage to 32 million uninsured people in the United States. The ACA had two major components: expansion of the

___________________

4 Federal law requires that state Medicaid programs make DSH payments to qualifying hospitals that serve a large number of Medicaid and uninsured people. Federal law establishes an annual DSH allotment for each state that limits federal financial participation (FFP) for total statewide DSH payments made to hospitals. Federal law also limits FFP for DSH payments through the hospital-specific DSH limit. Under the hospital-specific DSH limit, FFP is not available for state DSH payments that are more than a hospital’s eligible uncompensated care cost, which is the cost of providing inpatient hospital and outpatient hospital services to Medicaid patients and the uninsured minus payments received by the hospital by or on behalf of the patients in question (see https://www.medicaid.gov/medicaid/financing-and-reimbursement/dsh/index.html, accessed February 5, 2018).

Medicaid program and new structures to support the individual and small-group health insurance markets.

The ACA eliminated the concept of categorical eligibility and replaced it with standard eligibility criteria of 138 percent of the federal poverty level. In 2012, the Supreme Court ruled that the federal government could not force the states to expand Medicaid coverage. As a result, only 32 states and the District of Columbia elected to expand Medicaid (KFF, 2017b).

For the individual and small-group markets, the ACA established health insurance exchanges in states to allow individuals and small groups to buy standard insurance policies with income-based subsidies from 138 percent up to 400 percent of the federal poverty level (KFF, 2015b). The ACA eliminated medical underwriting and imposed a legal mandate to purchase health insurance with a penalty for those who did not comply. Before the ACA, insurance companies used medical underwriting to determine whether to offer a person coverage, at what price, and with what exclusions or limits based on the person’s health status; the purpose was to ensure a healthy risk pool by requiring people to pay premiums that reflected their expected medical costs. Because of medical underwriting in the individual and small-group markets, people who were sick often paid higher premiums or were denied coverage. The ACA’s individual mandate, in contrast, was designed to compel healthier people to purchase insurance so as to balance the risk pool and lower premiums for everyone. States could establish their own health insurance exchanges or use the one created by the federal government. However, access to care (except for increases in insurance coverage) did not show improvement until the time period between 2014 and June 2017 (KFF, 2017c).

THE HEALTH-CARE DELIVERY SYSTEM BEFORE THE PATIENT PROTECTION AND AFFORDABLE CARE ACT

The health-care delivery system in the United States consists of an array of clinicians, hospitals and other health-care facilities, insurance plans, and purchasers of health-care services, all operating in various configurations of groups, networks, and independent practices (IOM, 2003). The health-care delivery system has historically been organized around the concept of fee-for-service medicine. Under the fee-for-service payment model, patients (or their insurers) pay physicians and hospitals for any covered services delivered on a per-unit basis without particular regard for price, patient outcomes, or quality. Because provider revenues increase as more services are provided—and insured (and some uninsured) patients do not bear the full cost of the additional services—the fee-for-service model creates incentives to increase utilization of health-care services, which in many cases lead to overutilization of physician and hospital visits.

In some segments of the market, health plans have been designed around alternative incentive structures by using a concept of fixed payment for a set of services. Often called managed care, these plans aim to reduce overutilization of hospital and physician services through such arrangements as full-risk capitation payment models (which involve sharing of financial risk among all participants and place providers at risk not only for their own financial performance but also for the performance of other providers in the network), some forms of bundled payment (in which a single payment covers a hospital stay or all services related to a specific diagnosis or procedure), and a more modest approach called pay-for-value (an incentive structure that includes bonuses or penalties that are based on cost and quality metrics). Managed care is intended to reduce low-value spending through better “management” of care, but concerns have been raised about stinting and rationing in which high-cost–high-need patients are

not provided with care that is expensive but necessary. Pay-for-value managed-care arrangements are used in Medicare Advantage, Medicaid managed care, and some commercial health insurance plans.

In the Medicare program, around 30 percent of beneficiaries are enrolled in Medicare Advantage plans in which Medicare makes payments to private insurers that are responsible for delivering the Medicare benefit package, and payment arrangements between plans and providers are determined contractually and are thus difficult to describe because they are proprietary (KFF, 2017a).

In sharp contrast with Medicare, managed-care enrollment has greatly expanded during the past two decades, rising from just over one-half of all beneficiaries enrolled in managed care in 2000 to 77 percent in 2014 (KFF, 2014). Medicaid-managed care plans cover a broad array of Medicaid benefits, including acute, primary, and specialty care and in some states, behavioral health and LTSS (CMS, 2016).

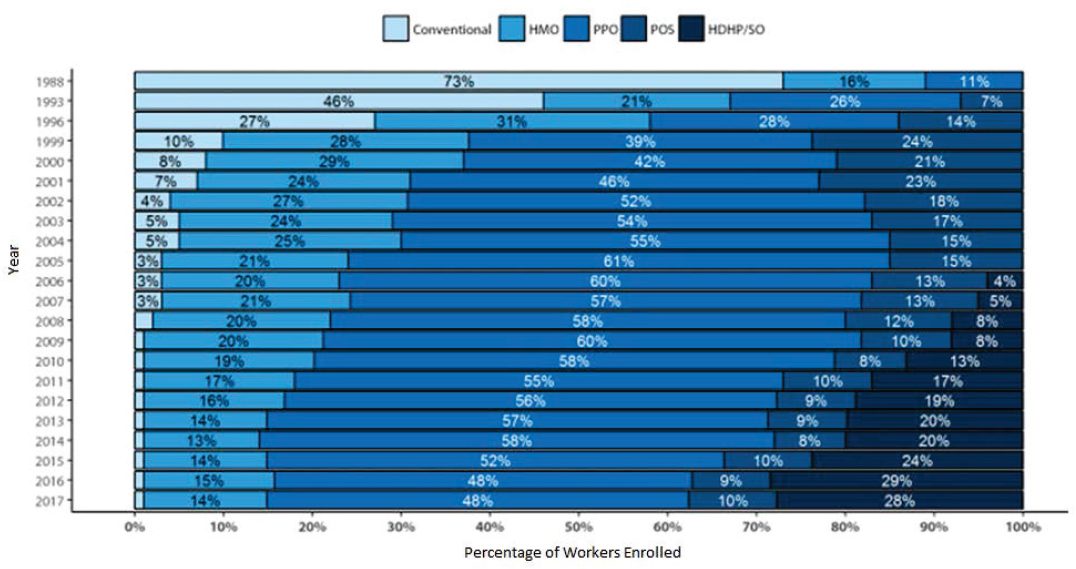

Although the fee-for-service model remains the most common payment form in the private health insurance market, private insurers have integrated aspects of the managed-care model into broader efforts to address the incentive problems created by the fee-for-service payment structure, such as utilization management and performance metrics for providers. If managed care is defined by the use of capitated payments to providers that are responsible for the total cost of care, then very few people are covered by managed care (KFF, 2016b). If, however, anything other than unconstrained fee-for-service is defined as managed care, most people who are covered by private health insurance are enrolled in some form of managed care. Managed care in any form usually involves restricting the set of providers from whom patients might obtain covered care to so-called in-network providers. Insurers can adjust network breadth to limit patient access to preferred hospitals and physicians. Figure 3-3 illustrates that dramatic shift over time. In 1998, 73 percent of employees enrolled in health plans had conventional fee-for-service coverage; by 2017, fewer than 1 percent had unconstrained fee-for-service coverage. The figure also shows the dramatic growth in HDHPs since 2006.

NOTES: Information was not obtained for POS plans in 1988 or for HDHP/SO plans until 2006. A portion of the change in plan type enrollment for 2005 is likely attributable to incorporating more recent Census Bureau estimates of the number of state and local government workers and removing federal workers from the weights. See the Survey Design and Methods section from the 2005 Kaiser/HRET Survey of Employer-Sponsored Health Benefits for additional information.

SOURCE: KFF, 2017d.

HOW THE PATIENT PROTECTION AND AFFORDABLE CARE ACT CHANGED THE HEALTH-CARE DELIVERY SYSTEM

The ACA included payment-reform provisions to incentivize the adoption of more effective care-delivery models (Abrams et al., 2015). The new models involve some combination of shared risk among providers to enhance collaboration and coordination of care so as to reduce avoidable hospitalizations, ED visits, and other forms of expensive or unnecessary care. To protect against stinting, quality metrics are often used to evaluate provider performance. Beyond payment models, the ACA encouraged (perhaps unintentionally) the narrowing of provider networks and reshaped the delivery of long-term services and supports, all of which have implications for the ways in which people who have disabilities receive care and for the documentation of that care in the medical record. Also relevant is the Health Information Technology for Economic and Clinical Health (HITECH) Act, which was enacted as part of the American Recovery and Reinvestment Act (ARRA) of 2009 and incentivized investments in electronic medical records (EMRs). We discuss each in turn.

New Payment and Delivery Models

One approach to payment reform under the ACA is “bundled payment,” whereby an insurer makes a single payment to a group of providers for all services that might be provided to a patient for a given medical condition or procedure. The payment, contractually determined in

advance, is intended to encourage better coordination among the various providers involved in a given patient’s care. Some 7,000 post-acute care providers, hospitals, and physician organizations have signed up to participate in bundled-payment demonstrations (Abrams et al., 2015). Early evidence suggests that bundled payments can reduce medical costs and improve patient satisfaction (CMS, 2017).

The ACA also incentivized the development of alternative delivery models, such as accountable care organizations. Those involve collaboration among physicians, hospitals, and other health-care entities in a shared-risk arrangement. The alternative delivery models were intended to encourage provider organizations to address patient health needs better, to reduce the amount of hospital and ED care, and to meet quality goals. Their effectiveness and their effects on clinical practice, however, are still matters of considerable debate (Schulman and Richman, 2016; Song and Fisher, 2016).

Another version of health-care delivery promoted by the ACA is the patient-centered medical home (PCMH). The primary goal of the PCMH is to keep people ambulatory in the community, in addition to aligning provider financial incentives with the best interests of patients. The PCMH is not a physical home but rather a care delivery system in which each patient’s care is coordinated through his or her primary care physician (PCP). The PCP manages and coordinates care with the goals of having each patient receive the necessary care when and where he or she needs it, and in a manner that the patient can understand and that is consistent with and respectful of the patient’s preferences, needs, and values (Blumenthal et al., 2015). In patient-centered models, there is greater potential for providers to identify people who have comorbidities and to coordinate their care. The National Committee for Quality Assurance (NCQA) reported in 2015 that PCMHs cut the growth in outpatient ED visits by 11 percent compared with non-PCMHs among Medicare patients. Visits for both ambulatory care sensitive and non-ambulatory care sensitive conditions were reduced; this suggests that steps taken by practices to attain PCMH recognition might decrease some of the demand for outpatient ED care (van Hasselt et al., 2015). NCQA also noted that PCMH recognition is associated with fewer inpatient hospitalizations and lower utilization of both specialist and emergency services (Harbrecht and Latts, 2012; Raskas et al., 2012).

Expanding Electronic Medical Records

The HITECH Act, enacted as part of the ARRA, encouraged the adoption of health technology in the form of EMRs. Money was offered to physician practices to meet compliance with health information technology or so-called meaningful use criteria or face penalties in Medicare reimbursement. EMRs offer the promise of aggregating records from many providers into a single, legible medical record as long as all providers seen by a patient participate in the same EMR system; interoperability among systems is imperfect. The HITECH Act offers the promise of a more complete medical record that details the full history of care provided to a patient who applies for disability benefits. But it is important to note that the Social Security Administration (SSA) listings are not structured to mirror how doctors use EMRs.

Narrowing Provider Networks

The change in provider network size is another indicator of how the ACA has transformed the care that people get. So-called narrow networks existed before the implementation of the ACA, but they have grown more common as a result of it. Many

consumer protection measures, such as the prohibition of medical underwriting, have made it difficult for many insurers to rely on traditional strategies to keep costs low. Other elements of the law, such as the availability of the online marketplace where consumers can compare premiums, have made it possible for insurers to compete with each other. Plans that have narrow networks might benefit consumers by lowering premiums. Negotiations between insurers and providers on network participation might encourage more efficient delivery of care. And the ability to contract selectively might allow insurers to attract a small group of providers that meet raised standards of quality and potentially would result in care of higher value (Health Affairs, 2016).

But narrow networks also pose risks to consumers. For example, if a network gets too narrow, it will jeopardize the ability of consumers to obtain needed care in a timely manner. That can also happen if the network contains an unsatisfactory mix or insufficient number of providers. Network limitations can have the additional effect of turning away sicker patients who have more health needs and thus changing the risk pool. One study notes that consumer advocates argue that narrow networks adversely affect access to care, especially for patients who have chronic illnesses. They claim that insurers structure the networks strategically to discourage the higher-cost patients from enrolling. Patients who have high needs will then have to go outside the network (and possibly outside the EMR system) and as a result tend to incur high expenses and receive surprise medical bills (EBRI, 2016). Their medical documentation is also more likely to be missing elements.

Reshaping Long-Term Care Services and Supports

The ACA included several provisions aimed at improving deficiencies in the nation’s long-term care system to ensure that people can receive LTSS in their home or the community (KFF, 2015a). In particular, the ACA expanded options for funding Medicaid home- and community-based services (HCBS). They include the Money Follows the Person Demonstration, the Balancing Incentive Program, the Section 1915(i) HCBS state plan option, and the Section 1915(k) Community First Choice state plan option. Those options have brought about a considerable increase in funds for Medicaid LTSS in the form of HCBS over the past two decades. HBSC increased from 53 percent of total Medicaid LTSS in FY 2014 to 55 percent in FY 2015 (Eiken et al., 2017).

In addition, in states that accepted the Medicaid expansion, funds were made available to pay for home- and community-based attendant services in connection with matching by the federal government (KFF, 2015a). Nonetheless, Wiener (2013) has argued that despite the growing need for HCBS, not enough progress had been made in improving the financing of long-term care. In particular, the Community Living Assistance Services and Supports (CLASS) Act under the ACA5 failed, making home-based LTSS insurance an expensive service that was out of reach for many Americans.

___________________

5 The Community Living Assistance Services and Supports Act (or CLASS Act) was a US federal law, enacted as Title VIII of the Patient Protection and Affordable Care Act. The CLASS Act would have created a voluntary and public long-term care insurance option for employees, but in October 2011 the Obama administration announced it was unworkable and would be dropped. The CLASS Act was repealed on January 1, 2013.

EFFECT OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT ON HEALTH-CARE UTILIZATION

A comprehensive review of the literature on the effects of the ACA Medicaid expansion on health-care use (KFF, 2017c) found that health insurance coverage has expanded overall, access to and use of care have increased, self-reported health status has improved, and flow of federal health-care resources into expansion states has risen.

It is less clear whether the ACA has altered utilization of EDs and hospitals. One study by Barakat et al. (2017) observed a substantial shift in payers for ED visits and hospitalizations after Medicaid expansion in California. It did not, however, detect a substantial change in top diagnoses or in the overall rate of ED visits and hospitalizations. The authors argued that there appeared to be a shift in reimbursement burden from patients and hospitals to the government without a dramatic shift in patterns of ED or hospital utilization. In contrast, Sommers et al. (2016) found that ED visits decreased and outpatient visits increased in Arkansas, Kentucky, and Texas after the ACA Medicaid expansion. Wherry and Miller (2016) observed an increase in office visits to physicians but also an increase in overnight hospital stays after the Medicaid expansion. Chen et al. (2016) noted that such minorities as blacks and Latinos, who were most affected by the ACA, experienced an even higher increase in care utilization than other groups.

There is consensus among studies on the effects of the ACA on utilization of preventive services. Sommers et al. (2016) found that use of preventive care, such as diabetes screening, increased. Similarly, Wherry and Miller (2016) found that Medicaid expansion under the ACA led to higher rates of preventive services, which resulted in more diagnoses of diabetes and high cholesterol.

Several studies have specifically identified ACA-related improvements in health-care utilization by people who had chronic conditions. Sommers et al. (2017a) examined changes in health-care use and self-reported health 3 years after the implementation of the ACA’s coverage expansion among people who had chronic conditions and had been uninsured but gained coverage. They found improvements in multiple measures: affordability of care, regular care for the chronic conditions, medication adherence, and self-reported health. A related study by Sommers et al. (2016) assessed changes in access to care, utilization, and self-reported health among low-income adults in three states that took alternative approaches to the ACA implementation. They echoed the findings in the 2017 report by suggesting that regular care for chronic conditions increased substantially after Medicaid expansion. The findings of those two studies were consistent with the findings of an earlier study by Sommers et al. (2015) that detected increases in self-reported health and functional status under the ACA in people who had chronic medical conditions.

Although evidence suggests that on average people who had chronic conditions experienced an increase in access to regular care for those conditions, coverage effects vary among diseases (Baicker et al., 2013), particularly as some states were much stricter in their underwriting regulations prior to the ACA. Because of the many design features that are common to the ACA, the Massachusetts health-care reform of 2006, and the Oregon Medicaid lottery of 2008, the experiences of Massachusetts and Oregon are informative about potential effects, and in particular long-term effects, of the ACA on utilization. A study by Cole et al. (2017) examined the random assignment embedded in the Oregon Medicaid lottery and found a greater probability of a diagnosis of diabetes and the use of medications for diabetes. It found no effect of Medicaid coverage on diagnoses or on the use of medication for blood pressure and

high cholesterol, but Cole et al. (2017), in a study of the ACA’s Medicaid expansion, found that coverage expansion was associated with better blood pressure control in community health center patients. The Oregon Medicaid study (Baicker et al., 2013) found substantial improvements in rates of diagnosis of and treatment for depression, which is strongly associated with disability.

The evidence on cancer care is also mixed. One study of the Massachusetts health-care reform did not find any changes in breast-cancer stage at diagnosis (Keating et al., 2013), but another found that the ACA’s dependent-coverage provision was associated with earlier-stage diagnosis of and treatment for cervical cancer, particularly in young women (Robbins et al., 2015). A third study of the Massachusetts reform echoed the improvement in cancer care by revealing that coverage expansion was associated with an increase in rates of treatment for colon cancer in low-income patients and a reduction in the number of patients waiting until the emergency stage for treatment (Loehrer et al., 2016).

In addition to health-care service utilization, the use of prescription drugs serves as an important measure of the ACA’s effect, especially given their prominent role in the management of chronic conditions. Mulcahy et al. (2016) found that those who had chronic conditions and gained insurance under the ACA filled an average of 28 percent more prescriptions and had a 29 percent reduction in out-of-pocket spending per prescription in 2014 compared with 2013. They attributed the increase in treatment rates for chronic conditions and the reduction in out-of-pocket spending to the decrease in financial barriers to care under the ACA. Sommers et al. (2017b) found that the first 15 months of expansion saw an increase in medication prescription rates, with the greatest increase seen in prescriptions for chronic conditions.

EFFECT OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT ON PEOPLE WITH DISABILITIES

The ACA has many provisions that are important for people who have disabilities. For example, denial of coverage because of pre-existing conditions is no longer allowed. Removal of a lifetime cap on benefits will enable people with disabilities to continue to receive care. Perhaps most important, the expansion of health insurance coverage through the Medicaid program, the health insurance exchanges, and the dependent coverage provision will allow many Americans who have disabilities to obtain health insurance coverage without having to qualify for SSDI or SSI. Those who qualify for Medicaid will have access to coverage for LTSS. And the ACA authorizes federally conducted or supported studies to collect standard demographic characteristics that include disability status (Krahn et al., 2015). In this section, we summarize the early literature on those effects.

The ACA’s dependent coverage provision appears to have benefited young adults who have disabilities. Porterfield and Huang (2016) analyzed the periods before and after implementation of the dependent coverage provision in the ACA and compared adults who had disabilities and were 19–25 years old with adults who had disabilities and were 26–34 years old. People in both age groups experienced coverage gains after the ACA dependent coverage provision took effect in 2010, but for people in the older group who were unaffected by the dependent coverage provision, the coverage gains were entirely attributable to changes in public insurance. In contrast, the coverage gains for people in the younger group who were affected by the dependent coverage provision were driven by changes in private insurance.

Sommers et al. (2014) found that an early Medicaid expansion in Connecticut resulted in substantially greater coverage gains for adults who had disabilities than for adults who did not. By 2014, low-income and moderate-income nonelderly adults—including both those who had and those who did not have chronic illnesses—also experienced coverage gains. The Kaiser Family Foundation (KFF, 2017c) notes that in some states and the District of Columbia, those gains resulted from the Medicaid expansion to adults who had incomes up to 138 percent of the federal poverty level. In other states and the District of Columbia, the coverage gains for people who had disabilities resulted from subsidies for qualified health plans offered on the health insurance marketplaces combined with private insurance reforms, such as the prohibition of discrimination based on health status.

The ACA appears to have brought about improvements in treatment for mental disorders and substance abuse. Saloner and LeCook (2014) examined the effect of the ACA on young adults who had mental health or substance-use disorders by using data from the 2008–2012 National Survey of Drug Use and Health. The authors found that after implementation of the ACA, mental health treatment of people who were 18–25 years old and had possible mental health disorders increased by 5.3 percent relative to that of a comparison group of similar people who were 26–35 years old. Uninsured visits by people who used mental health treatment decreased by 12.4 percent (the ACA helps by expanding mental health services, an ACA provision). Consistent with those findings, Ali et al. (2016) estimated that the ACA could make it possible for as many as 2.8 million adults to receive behavioral health treatment through the Medicaid expansions and another 3.1 million through participation in health insurance exchanges. If those possibilities are fully realized, that would represent a 40 percent increase in behavioral services utilization, primarily for mental health services. Golberstein et al. (2015) similarly found that the ACA’s dependent coverage provisions produced increases in general hospital psychiatric inpatient admissions, for substance use disorders and non-substance use psychiatric conditions, and higher rates of insurance coverage for young adults nationally, with the exception of visits to the ED in California.

A recent study (Hall et al., 2017) examined the effect of the Medicaid expansion on workforce participation by people who have disabilities. The authors noted that people who have disabilities often experience psychologic distress and comorbid health conditions and have low income and employment. New coverage options under Medicaid expansion that allow people to work more and accumulate assets could benefit people who have disabilities because they would no longer need to apply for SSI or live in poverty to qualify for Medicaid. Results from the Hall et al. study indicated that the number of adults who had disabilities and were employed increased in expansion states and decreased in nonexpansion states. Those changes were not statistically significant, because of the small sample in the pre-ACA period. However, after the ACA, those who had disabilities and lived in expansion states were more likely to be employed (38.0 percent versus 31.9 percent) and less likely to be unemployed than those who lived in nonexpansion states. The authors concluded that Medicaid expansion is an important policy for reducing disparities in access to care for people who have disabilities and for supporting their employment and financial independence.

Despite the many positive benefits of the ACA, there remain barriers to access to care among people who have disabilities. Among them is the complexity of the Medicaid application process (Gettens and Adams, 2015). Cost-related difficulties present another barrier. Despite the ACA’s subsidies for qualified health plans, which have reduced premium costs to some degree, deductibles and other out-of-pocket costs remain high and pose financial challenges to many

people who have disabilities (Gettens and Adams, 2015). A third concern related to the implementation of the ACA Medicaid expansion has been difficulties with respect to LTSS.

SUMMARY AND CONCLUSIONS

Health care in the United States is financed by a combination of public and private insurance, employers, and out-of-pocket payments by individuals. In 2015, 37 percent of the US population received health care through a public insurance program at some point during the year. The major public insurance systems are Medicare and Medicaid. In 2016, Medicare benefit payments totaled $675 billion and accounted for 15 percent of the federal budget.

The US health-care delivery system consists of an array of clinicians, hospitals and other health-care facilities, insurance plans, and purchasers of health-care services, all of which operate in various configurations of groups, networks, and independent practices. The healthcare delivery system historically has been organized around the concept of fee-for-service medicine. Under the fee-for-service payment model, patients (or their insurers) pay physicians and hospitals for any covered services delivered on a per-unit basis without particular regard for price, patient outcomes, or quality. Because provider revenues increase as more services are provided—and insured (and some uninsured) patients do not bear the full cost of the services—the fee-for-service model creates incentives to increase utilization of health-care services and leads in many cases to overutilization of physician and hospital visits.

The ACA was the largest federal health policy initiative since the creation of Medicare and Medicaid. It brought about structural changes in the health-care system, which included sweeping efforts to improve access to health insurance through expansion of the Medicaid program and through subsidized and lower-cost health insurance plans made available through new health insurance marketplaces (exchanges), elimination of pre-existing condition restrictions on coverage, elimination of lifetime caps on health-care spending, and efforts to slow growth in health-care costs through innovative payment reforms.

A major goal of the ACA was to extend health insurance coverage to 32 million uninsured people in the United States. The plan had two major components: expansion of the Medicaid program and new structures to support the individual and small-group health insurance markets. The ACA eliminated the concept of categorical eligibility and replaced it with standard eligibility criteria of 138 percent of the federal poverty level. In 2012, the Supreme Court ruled that the federal government could not force the states to expand Medicaid coverage. As a result, only 32 states and the District of Columbia elected to expand Medicaid.

For the individual and small-group markets, the ACA established health insurance exchanges in states to allow individuals and small groups to buy standard insurance policies with income-based subsidies from 138 percent to 400 percent of the federal poverty level. The ACA eliminated medical underwriting and imposed a legal mandate to purchase health insurance, with a penalty for those who did not comply. The ACA’s individual mandate was designed to compel healthier people to purchase insurance and thereby balance the risk pool and lower premiums for everyone.

The ACA included payment-reform provisions to incentivize the adoption of more effective care delivery models. The new models involve some combination of shared risk among providers to enhance collaboration and coordination of care in an effort to reduce avoidable hospitalizations, ED visits, and other forms of expensive or unnecessary care. To protect against stinting, quality metrics are often used to evaluate provider performance. Beyond payment

models, the ACA encouraged (perhaps unintentionally) the narrowing of provider networks and reshaped the delivery of LTSS, all of which have implications for how people who have disabilities receive care and the documentation of that care in the medical record.

The ACA has many provisions that are important for people who have disabilities. For example, denial of coverage because of pre-existing conditions is no longer allowed. The expansion of health insurance coverage through the Medicaid program, the health insurance exchanges, and the dependent coverage provision will allow many Americans who have disabilities to obtain health insurance coverage without having to qualify also for SSDI or SSI. Those who qualify for Medicaid will have access to coverage for LTSS.

A comprehensive review of the literature on the effects of the ACA Medicaid expansion on health-care use finds that health insurance coverage overall has expanded, access and use of care have increased, self-reported health status has improved, and the flow of federal health-care resources into expansion states has risen. It is less clear whether the ACA has altered utilization of EDs and hospitals.

REFERENCES

Abrams, M. K., R. Nuzum, M. A. Zezza, J. Ryan, J. Kiszla, and S. Guterman. 2015. The Affordable Care Act’s payment and delivery system reforms: A progress report at five years. New York: The Commonwealth Fund.

Ali, M. M., J. Teich, A. Woodward, and B. Han. 2016. The implications of the Affordable Care Act for behavioral health services utilization. Administration and Policy in Mental Health and Mental Health Services Research 43(1):11–22.

American College of Emergency Physicians. 2016. EMTALA: Main points. https://www.acep.org/News-Media-top-banner/EMTALA (accessed November 7, 2017).

Baicker, K., S. L. Taubman, H. L. Allen, M. Bernstein, J. H. Gruber, J. P. Newhouse, E. C. Schneider, B. J. Wright, A. M. Zaslavsky, A. N. Finkelstein, and G. Oregon Health Study. 2013. The Oregon experiment—effects of Medicaid on clinical outcomes. New England Journal of Medicine 368(18):1713–1722.

Barakat, M. T., A. Mithal, R. J. Huang, A. Mithal, A. Sehgal, S. Banerjee, and G. Singh. 2017. Affordable Care Act and healthcare delivery: A comparison of California and Florida hospitals and emergency departments. PLoS ONE 12(8):e0182346.

Blumenthal, D., M. Abrams, and R. Nuzum. 2015. The Affordable Care Act at 5 years. New England Journal of Medicine 372(25):2451–2458.

Brot-Goldberg, Z. C., A. Chandra, B. R. Handel, and J. T. Kolstad. 2017. What does a deductible do? The impact of cost-sharing on health care prices, quantities, and spending dynamics. The Quarterly Journal of Economics 132(3):1261–1318.

CBO (Congressional Budget Office). 2014. Veterans’ disability compensation: Trends and policy options. Washington, DC: CBO. https://www.cbo.gov/publication/45615 (accessed November 7, 2017).

CMS (Centers for Medicare & Medicaid Services). 2012. Emergency Medical Treatment and Labor Act (EMTALA). https://www.cms.gov/Regulations-and-Guidance/Legislation/EMTALA/index.html (accessed November 7, 2017).

CMS. 2016. Medicaid managed care enrollment and program characteristics, 2014. Baltimore, MD: CMS. https://www.medicaid.gov/medicaid-chip-program-information/by-topics/data-and-systems/medicaid-managed-care/downloads/2014-medicaid-managed-care-enrollment-report.pdf (accessed November 7, 2017).

CMS. 2017. Bundled Payments for Care Improvement (BCPI) initiative: General information. https://innovation.cms.gov/initiatives/bundled-payments (accessed November 7, 2017).

Cole, M. B., O. Galarraga, I. B. Wilson, B. Wright, and A. N. Trivedi. 2017. At federally funded health centers, Medicaid expansion was associated with improved quality of care. Health Affairs (Millwood) 36(1):40–48.

EBRI (Employee Benefit Research Institute). 2016. Issue brief no. 428: Narrow provider networks for employer plans. Washington, DC: EBRI. https://www.ebri.org/publications/ib/index.cfm?fa=ibDisp&content_id=3404 (accessed November 7, 2017).

Eiken, S., K. Sredl, B. Burwell, and R. Woodward. 2017. Medicaid expenditures for long-term services and supports (LTSS) in FY 2015. Truven Health Analytics. Bethesda, MD. https://www.medicaid.gov/medicaid/ltss/downloads/reports-and-evaluations/ltssexpendituresffy2015final.pdf (acessed February 5, 2018).

Gettens, J., and A. Adams. 2015. Assessing health care reform: Changes to reduce the complexity of the application process for individuals with disabilities. Journal of Disability Policy Studies 27(1):22–31.

Golberstein, E., S. H. Busch, R. Zaha, S. F. Greenfield, W. R. Beardslee, and E. Meara. 2015. Effect of the Affordable Care Act's young adult insurance expansions on hospital-based mental health care. American Journal of Psychiatry 172(2):182-189.

Hall, J. P., A. Shartzer, N. K. Kurth, and K. C. Thomas. 2017. Effect of Medicaid expansion on workforce participation for people with disabilities. American Journal of Public Health 107(2):262–264.

Harbrecht, M. G., and L. M. Latts. 2012. Colorado’s patient-centered medical home pilot met numerous obstacles, yet saw results such as reduced hospital admissions. Health Affairs (Millwood) 31(9):2010–2017.

Health Affairs. 2016. Health Affairs health policy brief: Regulation of health plan provider networks. Bethesda, MD: Health Affairs. https://www.healthaffairs.org/do/10.1377/hpb20160728.898461/full (accessed February 5, 2018).

IOM (Institute of Medicine). 2003. The future of the public’s health in the 21st century. Washington, DC: The National Academies Press.

Keating, N. L., E. M. Kouri, Y. He, D. W. West, and E. P. Winer. 2013. Effect of Massachusetts health insurance reform on mammography use and breast cancer stage at diagnosis. Cancer 119(2):250–258.

KFF (Kaiser Family Foundation). 2014. Total Medicaid managed care enrollment. https://www.kff.org/medicaid/state-indicator/total-medicaid-mc-enrollment (accessed November 7, 2017).

KFF. 2015a. Medicaid and long-term services and supports: A primer. Washington, DC: KFF. https://www.kff.org/medicaid/report/medicaid-and-long-term-services-and-supports-a-primer/view/footnotes (accessed November 7, 2017).

KFF. 2015b. The coverage provisions in the Affordable Care Act: An update. http://files.kff.org/attachment/issue-brief-the-coverage-provisions-in-the-affordable-care-act-an-update (accessed November 7, 2017).

KFF. 2016a. Total Medicaid spending FY 2016. https://www.kff.org/medicaid/state-indicator/total-medicaid-spending (accessed November 7, 2017).

KFF. 2016b. 2016 employer health benefits survey. https://www.kff.org/report-section/ehbs-2016-summary-of-findings (accessed November 7, 2017).

KFF. 2016c. Explaining health care reform: Risk adjustment, reinsurance, and risk corridors. https://www.kff.org/health-reform/issue-brief/explaining-health-care-reform-risk-adjustment-reinsurance-and-risk-corridors (accessed November 7, 2017).

KFF. 2017a. The facts on Medicare spending and financing. https://www.kff.org/medicare/issue-brief/the-facts-on-medicare-spending-and-financing (accessed November 7, 2017).

KFF. 2017b. Status of state action on the Medicaid expansion decision. https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act (accessed November 7, 2017).

KFF. 2017c. The effects of Medicaid expansion under the ACA: Updated findings from a literature review. Washington, DC: KFF. https://www.kff.org/medicaid/issue-brief/the-effects-of-medicaid-expansion-under-the-aca-updated-findings-from-a-literature-review-september-2017 (accessed November 7, 2017).

KFF. 2017d. 2017 employer health benefits survey. https://www.kff.org/report-section/ehbs-2017-section-5-market-shares-of-health-plans (accessed November 7, 2017).

Krahn, G. L., D. K. Walker, and R. Correa-De-Araujo. 2015. Persons with disabilities as an unrecognized health disparity population. American Journal of Public Health 105(Suppl 2):S198–S206.

Loehrer, A. P., Z. Song, A. B. Haynes, D. C. Chang, M. M. Hutter, and J. T. Mullen. 2016. Impact of health insurance expansion on the treatment of colorectal cancer. Journal of Clinical Oncology. 34(34):4110-4115.

Mulcahy, A. W., C. Eibner, and K. Finegold. 2016. Gaining coverage through Medicaid or private insurance increased prescription use and lowered out-of-pocket spending. Health Affairs (Millwood) 35(9):1725–1733.

Porterfield, S. L., and J. Huang. 2016. Affordable Care Act provision had similar, positive impacts for young adults with and without disabilities. Health Affairs 35(5):873–879.

Raskas, R. S., L. M. Latts, J. R. Hummel, D. Wenners, H. Levine, and S. R. Nussbaum. 2012. Early results show WellPoint’s patient-centered medical home pilots have met some goals for costs, utilization, and quality. Health Affairs (Millwood) 31(9):2002–2009.

Robbins, A. S., X. Han, E. M. Ward, E. P. Simard, Z. Zheng, and A. Jemal. 2015. Association between the Affordable Care Act dependent coverage expansion and cervical cancer stage and treatment in young women. JAMA 314(20):2189–2191.

Saloner, B., and B. Le Cook. 2014. An ACA provision increased treatment for young adults with possible mental illnesses relative to comparison group. Health Affairs (Millwood) 33(8):1425–1434.

Schulman, K. A., and B. D. Richman. 2016. Reassessing ACOS and health care reform. JAMA 316(7):707–708.

Sommers, B. D., G. M. Kenney, and A. M. Epstein. 2014. New evidence on the Affordable Care Act: Coverage impacts of early Medicaid expansions. Health Affairs (Millwood) 33(1):78–87.

Sommers, B. D., M. Z. Gunja, K. Finegold, and T. Musco. 2015. Changes in self-reported insurance coverage, access to care, and health under the Affordable Care Act. JAMA 314(4):366–374.

Sommers, B. D., R. J. Blendon, E. J. Orav, and A. M. Epstein. 2016. Changes in utilization and health among low-income adults after Medicaid expansion or expanded private insurance. JAMA Internal Medicine 176(10):1501–1509.

Sommers, B. D., B. Maylone, R. J. Blendon, E. J. Orav, and A. M. Epstein. 2017a. Three-year impacts of the Affordable Care Act: Improved medical care and health among low-income adults. Health Affairs (Millwood) 36(6):1119–1128.

Sommers, B. D., A. A. Gawande, and K. Baicker. 2017b. Health insurance coverage and health–what the recent evidence tells us. New England Journal of Medicine 377(6):586–593.

Song, Z., and E. S. Fisher. 2016. The ACO experiment in infancy—looking back and looking forward. JAMA 316(7):705–706.

USCB (US Census Bureau). 2016. Health insurance coverage in the United States: 2015. In Current Population Reports. Washington, DC: US Government Printing Office. https://www.census.gov/content/dam/Census/library/publications/2016/demo/p60-257.pdf (accessed November 7, 2017).

van Hasselt, M., N. McCall, V. Keyes, S. G. Wensky, and K. W. Smith. 2015. Total cost of care lower among Medicare fee-for-service beneficiaries receiving care from patient-centered medical homes. Health Services Research Journal 50(1):253–272.

Wherry, L. R., and S. Miller. 2016. Early coverage, access, utilization, and health effects associated with the Affordable Care Act Medicaid expansions: A quasi-experimental study. Annals of Internal Medicine 164(12):795–803.

Wiener, J. M. 2013. After class: The Long-Term Care Commission’s search for a solution. Health Affairs (Millwood) 32(5):831–834.