Coverage and Access:

Expanding Benefits to More Americans

Employer-sponsored insurance remains by far the single largest source of health insurance coverage in the United States, but coverage by employers has been eroding, even during periods of economic expansion. Meanwhile, increasing health care costs have constrained access to health care, especially for preventive services that have the potential to reduce overall health care spending. Government programs have countered these negative trends, but many people remain uninsured and lack ready access to health care, including undocumented immigrants and people of limited financial means.

1972

Updating Medicare

Medicare has protected Americans’ health and well-being since its inception, but two of its most impactful changes included expansions to cover even more individuals who needed it. In 1972, Medicare expanded for the first time to cover people with disabilities and people with end-stage renal disease who require dialysis or kidney transplant, providing a lifeline for these populations. Later, the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 added an optional prescription drug benefit known as Part D.

1985

Filling Gaps in Employer-Provided Insurance Coverage

The Consolidated Omnibus Budget Reconciliation Act of 1985 requires most employers to offer continuing health insurance coverage for a limited period of time to employees and their dependents who are no longer eligible for the company’s health insurance program. Enactment of the Health Insurance Portability and Accountability Act in 1996 extended the responsibility of health insurance coverage to benefit employees between jobs and helped protect patients from waste and fraud related to health insurance.

1993

Covering All Children

In response to a 1989–1991 measles epidemic in the United States where over half of the children infected had not been immunized, Congress created the Vaccines for Children program in 1993. The program provides vaccines at no cost to children who otherwise might not be vaccinated because of inability to pay. In 1997, the Children’s Health Insurance Program (CHIP) began providing federal matching funds to states to provide health coverage to children in families with incomes too high to qualify for Medicaid but too low to afford private coverage. All U.S. states have expanded coverage significantly through their CHIP programs, bringing more security to some of the nation’s most vulnerable children.

1996

Including Mental Health as Part of Whole-Person Health

The Mental Health Parity Act of 1996 barred separate annual and lifetime limits on coverage for the treatment of mental disorders other than addictions. While this did not address all restrictions on mental health benefits at the time nor apply to substance use disorder benefits, it was a foundational step in a growing movement to integrate mental, medical, substance use, and social services. Then, in 2008, the Mental Health Parity and Addiction Equity Act barred differential coverage limits and unequal application of managed care techniques for patients with mental illnesses and substance use disorders, greatly improving their lives.

2010s

Value-Based Health Care

Historically, the U.S. health care system has relied on fee-for-service compensation, where reimbursements are provided for each service provided regardless of the patient outcomes. Deficiencies in this model are clear, with the United States ranking highest in the world on health care spending yet lowest on health performance indicators among comparable nations. In recent years, and especially after the 2010 passage of the Patient Protection and Affordable Care Act, the Centers for Medicare & Medicaid Services has worked to address this problem by shifting toward value-based care, in which financial incentives are offered to physicians, hospitals, medical groups, and other health care providers for meeting certain performance measures and for developing innovative approaches to care.

2010

Expanding Health Insurance Coverage

The Patient Protection and Affordable Care Act of 2010 also mandated that health insurance providers accept all applicants without regard for pre-existing conditions or demographic status, except age; that insurers cover a list of essential health benefits, including mental health services and prescription drugs; and that all individuals in the United States acquire health insurance. As a result, the uninsured share of the U.S. population was cut roughly in half by 2016. The groups that have historically been at the greatest risk for lacking insurance—young adults, Latino(a)/Latinx/Hispanic communities, Blacks, and those with low incomes—have made the greatest gains in coverage.

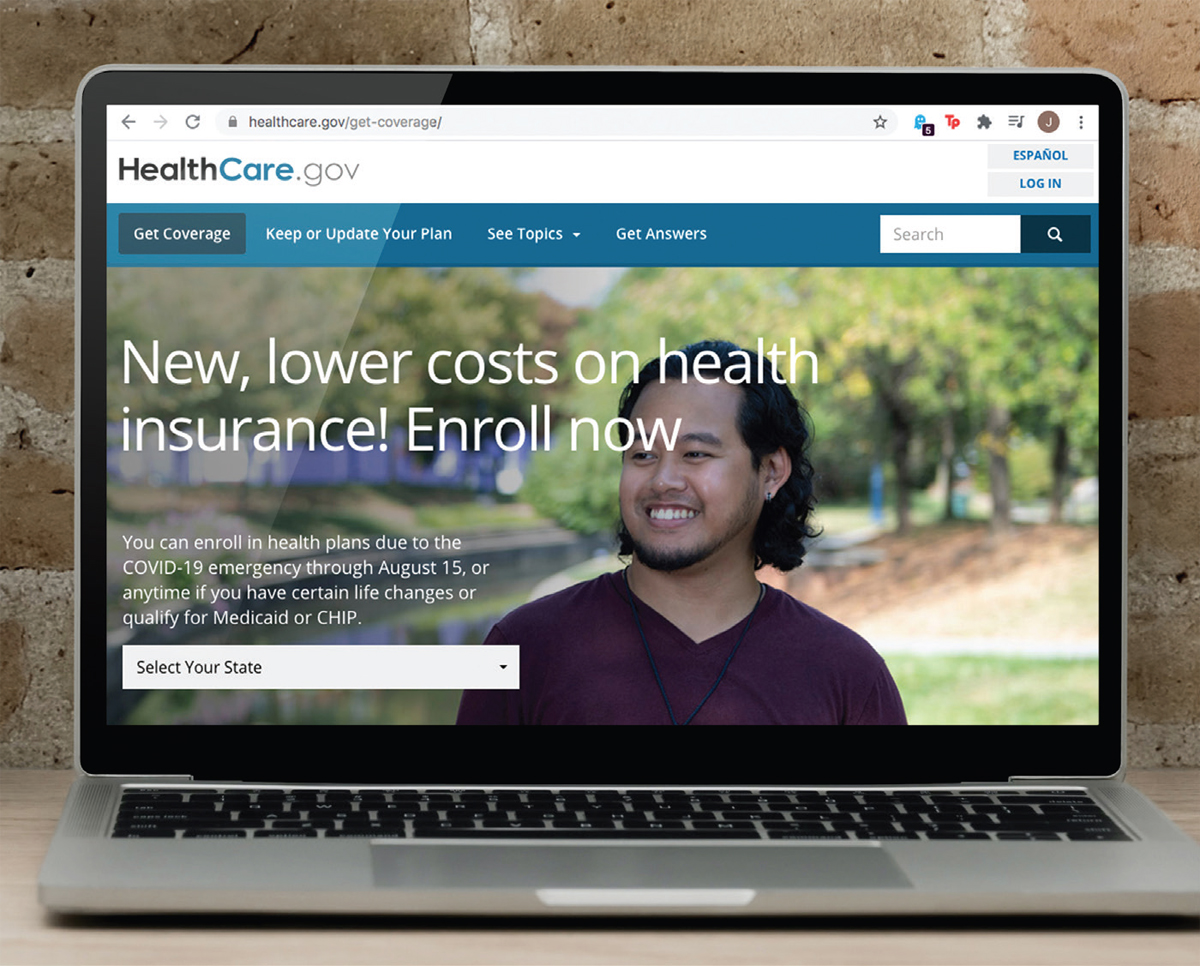

2013

Shopping for Affordable Insurance

After the Patient Protection and Affordable Care Act radically changed health insurance markets, enrollment in the Health Insurance Marketplace began in 2013. The marketplace helps people shop for and enroll in affordable health insurance through websites, call centers, and in-person assistance. The federal government operates the marketplace on behalf of most states. All state marketplaces can be conveniently accessed through the central location of HealthCare.gov.

2015

Paying for Value

In 2013, the Institute of Medicine report Best Care at Lower Cost: The Path to Continuously Learning Health Care in America was released, noting that approximately one-third of health care expenses were unnecessary, and recommending that the nation’s health system could be much more effective and efficient if available data, continuous improvement, and accountability standards were adopted.

Health insurance and access to health care have long been politically contentious issues, with proposed reforms ranging from modifications of the current system to single-payer systems. Regardless of the outcomes of these policy debates, an aging population, new and expensive medical treatments, and unanticipated events like the COVID-19 pandemic will continue to put pressure on both coverage and access.