G

Value, Benefits, and Risks

Federal facilities have value and generate benefits to society. Value generation and retention, as well as benefits, are always associated with some levels of risk. From enterprise risk management perspectives, a strategic view of risk management seeks to add value and focuses executive management on execution risks by (1) recognizing there is a relationship between taking risks and receiving benefits, (2) implementing risk management through strategies, and (3) establishing metrics and methods for evaluating performance of the risk management strategy.

From asset management perspectives, the International Organization for Standardization (ISO) 55000 incorporates risk management throughout by focusing on measures of value. Ultimately, measures of value are based on the delivery of products and services enabled by facilities. These measures of value cascade from organizational objectives to asset management objectives, then to asset performance and back again, to ensure and assure that key stakeholders get the value needed from facilities. This established the value determined by an organization based on its objectives and stakeholders (1) aligning asset management objectives with the organizational objectives, (2) using a life-cycle management approach to realize value from assets, and (3) establishing decision-making processes that reflect stakeholder need and define value.

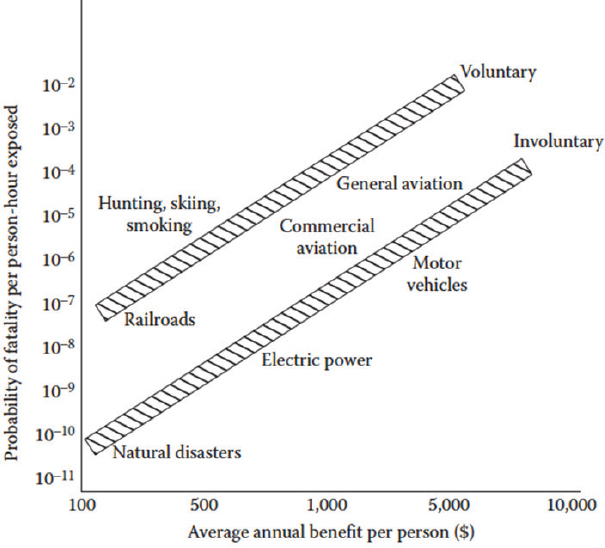

The method of revealed preferences, described at a high level in the next paragraph, provides a basis for comparing risks versus benefits and can be used to categorize different risk types. The underlying logic for this method and the relationship of interest is that decision makers do not take risks unless there is some benefit; otherwise, a rational decision maker will not undertake the risks, such as using future-proofing for federal facility renewal.

Benefits may be tangible or intangible, and measured in monetary or some other terms of worth, such as sustainability, pleasure, or symbolisms. Typically, different risk types can be segregated by voluntary versus involuntary actions or activities. The method of revealed preferences assumes that the society’s risk acceptance is a natural product of an equilibrium generated from historical experiences (or data) and predicted (or projected) information on risks versus benefits, including associated biases, subjectivity, and perceptions. The method generates inferred approximate lines (i.e., approximate thresholds) representing the acceptance of different activities, segregated by the voluntary/involuntary action categories. These lines are the revealed preferences. Further analysis of such revealed preferences leads to estimating the proportionality relationship between risk and benefit, which, if monetized, is typically quantified at about 1 unit of risk for about 1,000 units of benefit in engineering-related systems (Ayyub 2014a) (see Figure G-1). A more complete discussion of the revealed preferences method is outside the scope of this paper and may be found in Ayyub (2014a). Other disciplines, such as the medical field, might target different or significantly smaller benefit-to-risk ratios in cases such as the use of hazardous drug therapies.

SOURCE: Copyright 2014 from Risk Analysis in Engineering and Economics, 2nd ed., by B. Ayyub. Reproduced with permission from Taylor and Francis Group, LLC, a division of Informa PLC.

In the context of federal facilities, benefits may include operational efficiency, sustainment, public satisfaction, and image, all feeding into mission fulfillment. On the other hand, the risks may include loss of productivity, decrease in system sustainment, or economic inefficiency. Maintaining an associated balance between benefits and risks requires spending resources on system enhancement or renewals such as in the case of federal facilities. The allocation of these resources at the portfolio levels of federal facilities is essential in any strategy adopted by agencies.

The risks associated with deteriorating facilities vary by type, system, existing condition, function, utilization, and their relationship to an agency’s mission. Agencies can identify risks qualitatively, and some can be quantified, as illustrated in Chapter 3. Excess, underutilized, and obsolete facilities are a drain on the federal government’s budget in costs. They are forgone opportunities to invest in the maintenance and repair of mission-supportive facilities and to reduce energy use, water use, and greenhouse gas emissions. It is prudent for agencies to consider such impacts in analytical studies (NRC 2012b).

VALUE TYPES IN THE CONTEXT OF FEDERAL FACILITIES

Decision makers use risk studies to examine the potential loss of things that we value, such as goods, property, assets, people, and services. Many decision-analysis frameworks require valuations in economic, monetary, or other terms. Approaching economic value broadly from philosophy, particularly from ethics, one can make distinctions among the following value types: (1) instrumental and intrinsic values, (2) anthropocentric (i.e., human-centric) and biocentric (or ecocentric) values, (3) existence value, and (4) utilitarian and deontological values (Callicott 2004; NRC 2005b). A primary basis for the development of a renewal strategy of federal facilities is economic valuation; however, it is necessary to introduce and discuss these distinctions. A federal agency with a facilities portfolio and a mission to sustain a set of ecosystems will be used as an example to discuss these distinctions, where an ecosystem is a biological community of interacting organisms and their physical environment.

The federal facility addressing these ecosystems draws on, as an example, the instrumental value of these systems that is derived from their role as a means toward an end other than itself—that is, its value is derived from its usefulness in contributing toward a mission. A human-centric value system considers humankind the central focus or final goal of the universe, with humans being the only thing with intrinsic value. In this system, humans derive the instrumental value of everything else from its usefulness in meeting their needs. A biocentric value system (i.e., non-human-centric), assigns intrinsic value to all individual living systems, including but not limited to humans. This system assumes that all living systems have value even if humans cannot determine their usefulness or can be

harmed by them. Other considerations include the existence value system and the deontological value system.

The treatment offered in this report recommends the general use of a valuation approach with the following characteristics (Ayyub 2014a), with exceptions as necessary:

- Human-centric based on utilitarian principles;

- Consideration of all instrumental values, including existence value;

- Utilitarian basis to permit the potential for substitutability among different sources of values that contribute to human welfare;

- Individual preferences or marginal willingness to trade one good or service for another that can be influenced by culture, income level, and information, making it time and context-specific; and

- Societal values as the aggregation of individual values through a system of governance representing society at large.

The approach defined by this list is consistent with current recommended practices from the National Academies of Sciences, Engineering, and Medicine (NRC 2005b). It does not capture non-human-centric values—for example, biocentric values and intrinsic values. In some decisions, including environmental policy and law, the federal government does include biocentric intrinsic values, such as in the Endangered Species Act of 1973.

VALUE AND BENEFITS OF RENEWAL

Value generation requires a multidimensional representation as a matrix of stakeholders and their influence, wants, and needs, quantified through multiattribute decision-making processes; or stakeholder value can be reduced to a single number. The multiattribute decision-making processes may include weighting methodologies to enable prioritization of dimensions, factors, or attributes (ISO 2014c).

Federal agencies can achieve beneficial outcomes of renewal through timely investments in federal facilities maintenance, repair, replacement, or repurposing (NRC 2012b). Those outcomes support mission achievement, compliance with regulations, improved condition, efficient operations, and stakeholder-driven preferences as introduced in Chapters 1 and 2. Agencies can measure all of these outcomes. Some outcomes, including reliability and physical condition, are suitable for predictive and projective pursuits. Agencies can estimate these outcomes before making, or choosing not to make, an investment. Deteriorating facilities and systems pose risks to the federal government, its agencies, workforce, and the public, including risks to the achievement of federal agencies’ missions; risks to safe, healthy, and secure workplaces; risks to the government’s fiscal soundness; risks to efficient and cost-effective operations; and risks to achieving public policy objectives. Table G-1 provides a summary of these beneficial outcomes related to investments in maintenance and repair.

TABLE G-1 Summary of Beneficial Outcomes Illustrated for Investments in Maintenance and Repair

| Mission-Related Outcomes | Compliance-Related Outcomes | Condition-Related Outcomes | Efficient Operations | Stakeholder-Driven Outcomes |

|---|---|---|---|---|

| Improved reliability | Fewer accidents and injuries | Improved condition | Less reactive, unplanned maintenance and repair | Customer satisfaction |

| Improved productivity | Fewer building-related illnesses | Reduced backlog of deferred maintenance and repairs | Lower operating costs | Improved public image |

| Functionality | Fewer insurance claims, lawsuits, and regulatory violations | Lower life-cycle costs | ||

| Efficient space utilization |

Cost avoidance

Reduced energy use Reduced water use Reduced greenhouse gas emissions |

SOURCE: National Academies of Sciences, Engineering, and Medicine, 2012, Predicting Outcomes of Investments in Maintenance and Repair of Federal Facilities, Washington, DC: The National Academies Press, https://doi.org/10.17226/13280.

The value derived from assets varies over the life of the assets (see examples below) requiring the tracking of factors that influence value generation.

- During the investment or acquisition stage, assets are costs to the organization, but have value generated once in operation, with tension arising among asset acquisition, upkeep, repurposing, etc.

- Some assets can have a time delay before generation of value.

- At times, circumstances can lead private organizations to price outputs at a price point that ignores the original acquisition cost.

- Functional obsolescence due to changes in technology or changes in organizational objectives can mean that an asset will change its value to the organization.

- Consumer or stakeholder preferences may change over time (ISO 2014c).

ECONOMIC VALUATION

Economic valuation is defined as the worth of a good or service as determined by the markets. Economic valuation provides a basis for and is often used in decision analysis as discussed in Chapter 4. Economists initially dealt with this concept by estimating a good’s value to an individual, then extending it broadly as it relates to markets for exchange between buyers and sellers for wealth maximization. Traditionally, the value of a good or service is linked to its price in an open and competitive market, determined primarily by the demand relative to supply. Therefore, goods, property, assets, safety, security of people, or services are treated as commodities. If there is no market to set the price of a commodity, then it has no economic value. Therefore, the value refers to the market worth of a commodity, which is determined by the equilibrium at which two commodities are exchanged. The limitation is in its inability to set a value of things that are not exchanged in markets.

The concept of economic valuation is rooted in the labor theory of value. The theory states that a good or service is related to the amount of discomfort or labor saved through the consumption or use of it. According to this theory, the exchange value is recognized without making it equivalent to an economic value—price and value are considered two different concepts. A value is determined based on the exchange price that does not necessarily represent its true economic value.

An economic measure of a good’s value or a service’s benefit is the maximum amount a person will pay for the good or service. The concept of willingness to pay (WTP) is central to economic valuation. An alternative measure is the willingness to accept (WTA), the amount a person will accept to forgo a good. One would expect WTP and WTA to produce similar amounts; however, WTA amounts are typically greater than WTP amounts, primarily because of income levels and affordability factors. These concepts offer bases for economic valuation of services necessary for market-driven enhancements of conditions of facilities. Chapter 3 introduces notions on condition-index or level-of-service analysis.

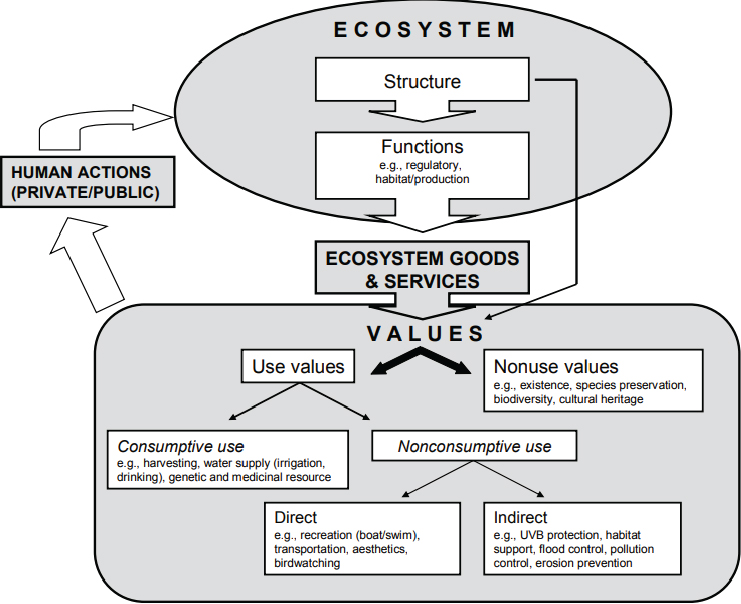

The economic concept of value, including exchange value, is well accepted. The concept of total economic value offers a broad basis to account for other considerations that do not have explicit or direct market value, as illustrated in Figure G-2.

CONSISTENCY IN RISK ANALYSIS AND MANAGEMENT

A strategy to renew federal facilities should be rooted in meeting missions of agencies, economic values, benefits, potential losses, cost effectiveness, and cost efficiency.

SOURCE: National Research Council, 2005, Valuing Ecosystem Services: Toward Better Environmental Decision-Making, Washington, DC: The National Academies Press, https://doi.org/10.17226/11139.

Requirements for Risk Frameworks

Risk management entails resource allocation. The use of an economic framework, building on economic valuation and monetization of value and benefits, offers a basis for consistency and rationality in decision making. This section sets requirements for appropriate risk frameworks based on best practices.

As introduced in Chapter 2, OMB Circular A-123 defines an agency’s responsibilities for enterprise risk management and internal control. It also guides federal managers to improve accountability and effectiveness of federal programs and mission-support operations by implementing enterprise risk management practices and establishing, maintaining, and assessing internal control effectiveness. The Circular emphasizes the need to integrate and coordinate risk management and effective internal control into existing business activities as an integral part of managing an agency.

Kaplan and Garrick (1981) captured the essence of risk assessment as applied to facilities and building system components in three questions posed originally for risk assessment of nuclear reactors (NRC 2012b):

- What can go wrong?

- What are the chances that something with serious consequences will go wrong?

- What are the consequences if something does go wrong?

Renewing federal facilities requires the development of a decision framework customized to meet the needs of a federal agency by meeting the following set of requirements to achieve consistency across agencies with resilience-related considerations (Ayyub 2014b), as discussed further in Chapter 3. A decision framework customized for a federal agency

- Builds on accepted definitions for uncertainty, risk, decision, and economic analysis;

- Considers the initial and desired future capabilities and capacities in terms of quantifiable performances;

- Treats capabilities, capacities, and performances as time variant with appropriate and justifiable projections and degradations within a planning horizon;

- Considers potential hazards and disturbances as sources of harm with occurrence rates and intensity treated probabilistically;

- Permits the characterization of performance in multidimensions with the associated things at risk, such as people, physical infrastructure, economy, key government services, social networks and systems, and environment;

- Accounts for systems changes over time, in some cases being improved, in other cases growing more fragile or aging;

- Accounts for full or partial recovery and times to recovery for enhancing functional and operational resilience;

- Accounts for potential enhancements to system performance after recovery from an adverse event or in response to other needs;

- Provides for the use of real options and associated economics in order to meet projected needs with deep uncertainty, such as hazards associated with a changing climate;

- Relates outcomes to other familiar notions such as reliability and risk;

- Incorporates uncertainty analysis probabilistically; and

- Requires input with meaningful units, is unit-consistent, and produces results with meaningful units.

ISO 55000 identifies the need to balance cost, risk, and performance in the generation of value with corresponding implications as follows:

- Cost usually needs to be controlled in order to generate value for the organization by maintaining financial viability. Time shifting of either costs or value generation can play a major role in managing financial viability; for example, some public service providers cross-subsidize services by using revenue from high-density population areas to help fund services to what would otherwise be unviable in sparsely populated areas.

- The likelihood or consequence of a threat is reduced, or the likelihood of or return from an opportunity to enhance value generation is increased.

- Performance is linked to success in generating value or meeting the asset management objectives (ISO 2014c).

Risk Analysis and Management Frameworks

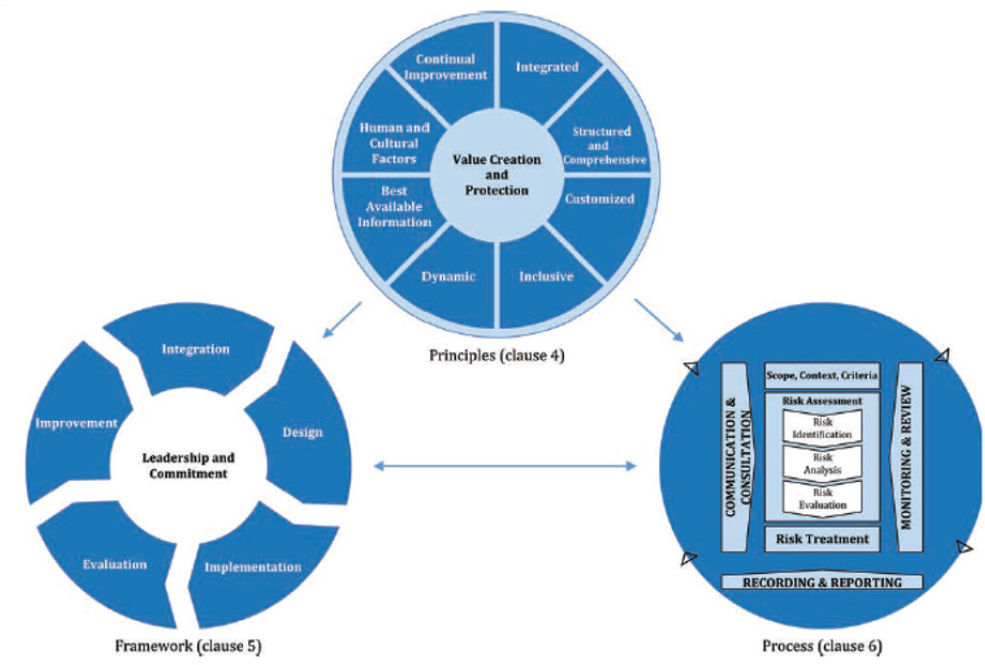

Treatment of risk is a complex issue that must be considered in every decision-making activity. This is addressed in ISO 55000 and ISO 55001, which apply guidance from ISO 31000 supporting the implementation of asset management systems. Figure G-3 provides an example framework for risk analysis and management that meets the requirements outlined in the previous section.

In practice, formulaic risk methodologies are generally not robust enough for federal facility asset management systems covering whole portfolios. Therefore, it is best to approach implementation of risk management techniques through frameworks, principles, and processes, as represented in Figure G-3, and as detailed in the discussion on facility asset management principles in Appendix F.

SOURCE: © ISO. This material is reproduced from ISO 31000:2018 with permission from the American National Standards Institute (ANSI) on behalf of the International Organization for Standardization. All rights reserved.