Appendix B

Benchmark Levelized Cost of Electricity Estimates

Evaluation of policies for market adoption of clean energy for electricity generation begins with a view of the economic competitiveness of alternative technologies. Although the details will vary for myriad reasons for any particular installation, benchmark numbers are available to indicate the relative magnitude of delivered energy costs. The Energy Information Administration (EIA) has long experience and provides substantial supporting information regarding cost estimates used in the National Energy Modeling System (NEMS) and applied in the Annual Energy Outlook (AEO). This appendix summarizes the essential elements for consistent cost estimates as applied in AEO2016.

EQUIVALENT GENERATION COSTS

The NEMS includes a series of components that utilize information about the various contributions to the cost of electricity generation. The levelized cost of electricity (LCOE) is a summary benchmark statistic based on the elements in the NEMS:

Levelized cost of electricity (LCOE) is often cited as a convenient summary measure of the overall competiveness of different generating technologies. It represents the per-kilowatt hour cost (in real dollars) of building and operating a generating plant over an assumed financial life and duty cycle. Key inputs to calculating LCOE include capital costs, fuel costs, fixed and variable operations and maintenance (O&M) costs, financing costs, and an assumed utilization rate for each plant type. The importance of the factors varies among the technologies. For technologies such as solar and wind generation that have no fuel costs and relatively small variable O&M costs, LCOE changes in rough proportion to the

estimated capital cost of generation capacity. For technologies with significant fuel cost, both fuel cost and overnight cost estimates significantly affect LCOE. The availability of various incentives, including state or federal tax credits, can also impact the calculation of LCOE. As with any projection, there is uncertainty about all of these factors and their values can vary regionally and across time as technologies evolve and fuel prices change. (EIA, 2015f, p. 1)

The AEO supporting information identifies the methodology and assumptions that affect the reported estimates of LCOE for utility-scale generation technologies. The reported estimates are for the years 2022 and 2040. The focus here is on the 2022 estimates as the benchmark for the “current” costs. The assumptions include choices regarding the effects of learning, capital costs, transmission investment, operating characteristics, and externalities. These choices are both important and appropriate for the benchmark comparison (e.g., learning rates), are important and require some adjustment (e.g., capital costs), or are supplemental to the EIA assumptions (e.g., externality costs).

LEARNING RATES

The cost estimates include detailed construction of the components of overnight capital cost of investment (EIA, 2013d). An important feature of the capital cost estimates reflects the maturity of the technology. For mature technologies, such as conventional coal, there is a minimum exogenous annual cost reduction. For newer technologies, such as wind and solar, the technologies have different learning rates in the range of 1-20 percent (EIA, 2015b, p. 107). For the first four units of a technology, there is an assumed increase in the costs above the base cost estimate to capture the effect of first-of-a-kind units. The learning rates applied to the base cost estimates decline after the first three and subsequent five doublings of installed capacity. The cost of competing technologies increases, particularly for natural gas. The result is a different ranking of the technologies in 2040 than in 2022, with renewables being more competitive in 2040.

CAPITAL CHARGES

The NEMS model supports many purposes, from projection to analysis. For projection applications, a constant issue arises as to what policies to assume for the future. In general, the practice is to assume that existing law would determine future policies. Hence, if there is a production tax credit for wind that

is scheduled to expire before 2022, it is not included in the 2022 estimates, even though the tax credit has been renewed many times before.

This is an appropriate compromise regarding policy assumptions for projection. However, in constructing a benchmark for comparing the underlying competitiveness of technologies, the starting point should be the cost estimates without included policies that selectively target technologies. Ideally, the levelized cost estimates would be computed in a way that eliminates the impact of policies that cause market distortions, such as those that preferentially subsidize one technology or a class of technologies over others. A second-best option would be to include the effects only of policies that are technology-neutral, such as the income tax.

The cost estimates in AEO2016 include two important assumptions reflecting selective policies that affect the capital cost estimates. First, the weighted average cost of capital (WACC) is 5.6 percent in real terms. But for new coal plants, there is an additional 3 percent added to proxy for anticipated carbon restriction policies (EIA, 2015f, p. 3). Second, certain technologies, particularly wind and solar, use accelerated tax depreciation that is not available to other technologies. This produces substantially lower fixed-charge rates for renewable capital costs.1

Without these selective polices, the fixed-charge rates would be closer and reflect only real differences in component costs and lead times for production that affect capital costs. The assumed lead times for the technologies appear in the AEO assumptions (EIA, 2015b, p. 105). The capital charge rates applied here are for the comparable fossil fuel technology that has the same lead time. Thus the capital costs reported differ from those in EIA (2015f) in removing the 3 percent premium for coal and the accelerated depreciation for selected technologies.

TRANSMISSION INVESTMENT

In general, the technologies differ in terms of the transmission investment required to serve the final load. Potential wind and solar capacity factors can differ substantially by location. Often a wind or solar resource is geographically distant from the demand load and necessitates a transmission investment, such as an upgrade to existing infrastructure or a new transmission line. In contrast, a natural gas or coal power plant can usually be sited as close to the demand load as possible, given other factors such as the cost of land and social factors. Even in the case of local versus distant renewables, there is a well-recognized tradeoff between optimal performance of the renewables and the cost of transmission investment (Midwest ISO, 2010). AEO2015 incorporates estimates of the

___________________

1 Personal communication, EIA, spreadsheet AEO2014_financial.xls.

required transmission investment, and these costs are included in the LCOE (EIA, 2015f, p. 6).

DISPATCH PROFILES

EIA separates electricity generation technologies into categories of dispatchable and nondispatchable (EIA, 2015f, p. 6). The former include conventional fossil fuel plants that have a fairly consistent available capacity and can follow dispatch instructions to increase or decrease production. The latter consist of intermittent plants such as wind and solar, which depend on the availability of the wind and sunlight and typically cannot follow dispatch instructions easily or at all. It is generally recognized that the different operating profiles create different values for the technologies (Borenstein, 2012; Joskow, 2011). Empirical estimates for existing technologies show that the value of wind, which blows more at night when prices are low, can be 12 percent below the unweighted average price of electricity; and the value of solar, with the sun tending to shine when prices are higher, can be 16 percent greater than the unweighted average (Schmalensee, 2013).

One procedure utilized for putting nondispatchable technologies on an equivalent basis is to pair them with appropriately scaled dispatchable peaking technologies to produce an output that is like that of a conventional fossil fuel plant (Greenstone and Looney, 2012). Another approach, used by Schmalensee (2013), is to calculate the value of nondispatchable technologies based on spot prices. EIA provides a similar estimate based on its projected simulations, which is known as the levelized avoided cost estimate (LACE):

Conceptually, a better assessment of economic competitiveness can be gained through consideration of avoided cost, a measure of what it would cost the grid to generate the electricity that is otherwise displaced by a new generation project, as well as its levelized cost. Avoided cost, which provides a proxy measure for the annual economic value of a candidate project, may be summed over its financial life and converted to a stream of equal annual payments. The avoided cost is divided by average annual output of the project to develop the “levelized” avoided cost of electricity (LACE) for the project. (EIA, 2015f, p. 2)

For purposes of equivalent comparison of the LCOE, the approach here combines these adjustments to provide an estimate of the net difference between the LACEs for the technology and for a conventional combined-cycle natural gas plant. The net differences are added to (e.g., for wind) or subtracted from (e.g., for solar) the other components of the LCOE.

EXTERNALITIES

The LCOE excluding marginal externalities provides a benchmark for comparison. However, a central point of the consideration of clean energy technologies is the impact of externalities. Hence, in addition to the equivalent cost estimates absent policies for pricing externalities, the estimates here incorporate separate components for the major externalities.

The principal externalities for electricity generation include the criteria pollutants and carbon dioxide (CO2). The supporting documents for AEO2016 provide emission rates and associated heat rates (EIA, 2013d, pp. 2-10). For the criteria pollutants—such as sulfur dioxide, nitrogen oxide, and small particulates—the externality values are highly dependent on location because of different exposure effects, and are difficult to quantify with a benchmark value. However, the basic story for noncarbon externalities is relatively simple. The impacts are an order of magnitude larger for coal than for natural gas. By one estimate, the noncarbon health impacts for coal are greater than the value added of the coal sector (Muller et al., 2011). For illustrative purposes, however, the estimates here include the noncarbon damages for coal and natural gas plants from Greenstone and Looney (2012), using the emission rates of the criteria pollutants.

For carbon, the locational differentials do not pose any difficulty because of the nature of the global effects of emissions anywhere. Here emission rates by technology type come from the heat rate and emission data in AEO2016 (EIA, 2013d).2 The price of carbon is set at the round number of $15/ton of CO2, taken as representative of the 3 percent discount case of the Interagency Working Group on Social Cost of Carbon (2013). Note that this is a global externality cost estimate. Looking only at the damages for the United States would reduce the social cost by about an order of magnitude. The $15 figure is selected as a round number to make it easy to convert the graphic for other arguable values of the appropriate prices of carbon.

LEVELIZED COST OF ELECTRICITY

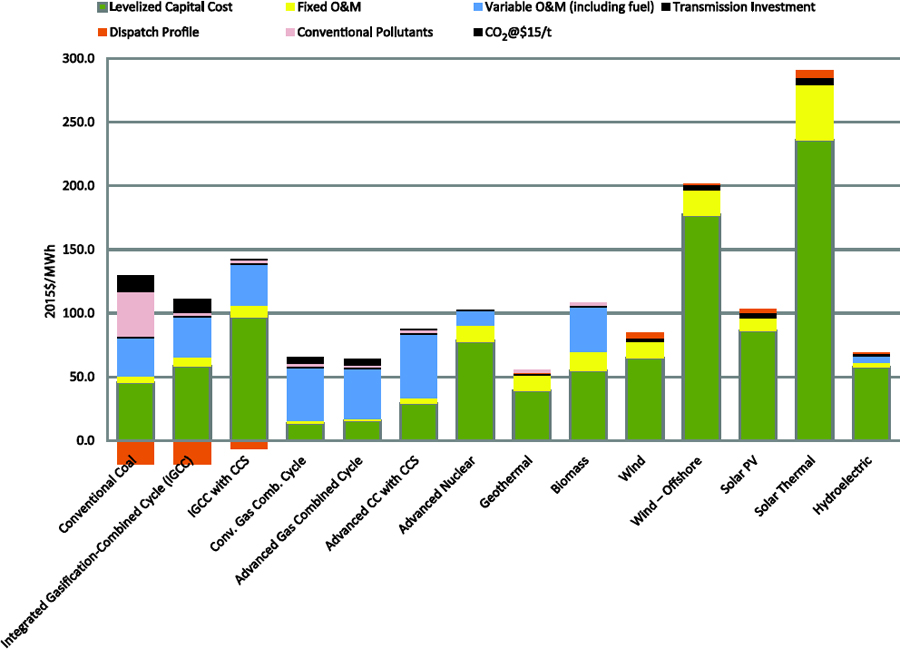

With the above assumptions and adjustments to obtain an approximation of equivalent LCOE, the results appear in Figure B-1 and Table B-1.

It is clear from Figure B-1 that new natural gas plants are the dominant technology. And without accounting for the costs of externalities, new IGCC

___________________

2 The EIA data show carbon emissions for biomass and geothermal. The NEMS model assumes zero carbon emissions, presuming that biomass fuel recycles the carbon. Geothermal is treated here as zero-carbon.

SOURCE: EIA, 2015f, 2016g. Because Annual Energy Outlook 2016 does not assess conventional coal and IGCC technologies, their values (in 2013 dollars) were sourced from Annual Energy Outlook 2015 and then converted to 2015 dollars using the Bureau of Economic Analysis’ gross domestic product (GDP) implicit price deflator.

coal plants are more competitive than even the best of the wind and solar. Onshore wind is the closest to being competitive. But the relative cost estimates shown here are similar to those in Greenstone and Looney (2012). The primary renewable technologies are not cost-competitive, and the differences are significant. This is for entry year 2022. Looking ahead to 2040, with some additional cost reductions for renewables and more substantial increased fuel costs for natural gas, the situation changes for wind but not for solar.

TECHNOLOGY ADOPTION

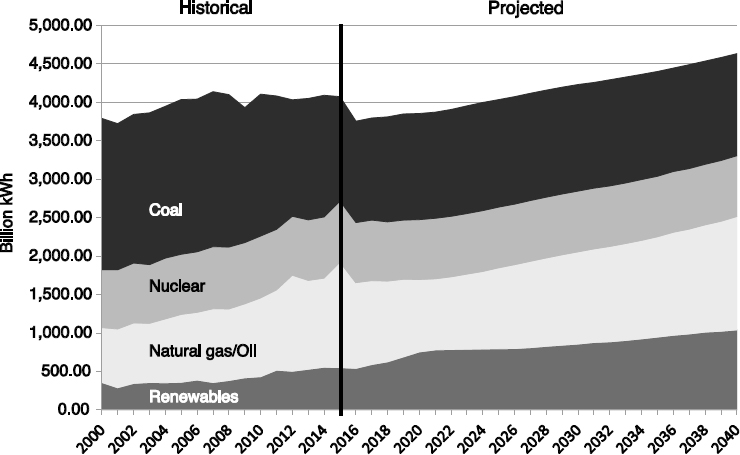

The EIA projections include many factors other than the implied LCOE. For example, although geothermal and conventional hydroelectric technologies are among the most cost-competitive, their penetration is limited because of constrained resources. The AEO2016 Reference Case shows the projected growth in electricity generation and the relative role of the various

TABLE B-1 Summary of Levelized Cost of Electricity (LCOE) for Year 2022 Entry (2015 $/MWh)

| Plant Type | Levelized Capital Cost | Fixed Operations and Maintenance (O&M) Costs | Variable O&M Costs (including fuel) | Transmission Investment | Dispatch Profile | Criteria Pollutants | CO2 @ $15/ton | Total System Average LCOE |

|---|---|---|---|---|---|---|---|---|

| Conventional Coal | 45.9 | 4.3 | 30.2 | 1.2 | -18.2 | 35.0 | 12.3 | 111.0 |

| Integrated GasificationCombined Cycle (IGCC) | 58.4 | 7.1 | 31.5 | 1.2 | -18.2 | 2.0 | 10.5 | 92.6 |

| IGCC with Carbon Capture and Storage (CCS) | 97.2 | 9.2 | 31.9 | 1.2 | -6.5 | 2.0 | 1.2 | 136.2 |

| Conventional Gas Combined Cycle | 13.9 | 1.4 | 41.5 | 1.2 | 0.0 | 2.0 | 5.4 | 65.5 |

| Advanced Gas Combined Cycle | 15.8 | 1.3 | 38.9 | 1.2 | 0.0 | 2.0 | 5.1 | 64.3 |

| Advanced Combined Cycle with CCS | 29.2 | 4.3 | 50.1 | 1.2 | 0.0 | 2.0 | 0.6 | 87.5 |

| Advanced Nuclear | 78.0 | 12.4 | 11.3 | 1.1 | -0.3 | 0.0 | 0.0 | 102.5 |

| Geothermal | 38.9 | 12.6 | 0.0 | 1.4 | 0.2 | 2.0 | 0.0 | 55.2 |

| Biomass | 54.7 | 14.9 | 35.0 | 1.2 | -0.1 | 2.0 | 0.0 | 107.8 |

| Wind | 64.6 | 13.2 | 0.0 | 2.8 | 4.4 | 0.0 | 0.0 | 85.0 |

| Wind—Offshore | 177.0 | 19.3 | 0.0 | 4.8 | 0.2 | 0.0 | 0.0 | 201.3 |

| Solar Photovoltaic (PV) | 86.2 | 9.9 | 0.0 | 4.1 | 2.9 | 0.0 | 0.0 | 103.1 |

| Solar Thermal | 235.9 | 43.3 | 0.0 | 6.0 | 5.6 | 0.0 | 0.0 | 290.8 |

| Hydroelectric | 57.5 | 3.6 | 4.9 | 1.9 | 0.9 | 0.0 | 0.0 | 68.8 |

SOURCE: EIA, 2015f, 2016g. Because Annual Energy Outlook 2016 does not assess conventional coal and IGCC technologies, their values (in 2013 dollars) were sourced from Annual Energy Outlook 2015 and then converted to 2015 dollars using the Bureau of Economic Analysis’ gross domestic product (GDP) implicit price deflator.

technology groupings (see Figure B-2). Importantly, the total growth of electricity is modest by historical standards, and this inhibits the introduction of new technology.

In part, the renewable growth is driven by implicit policies, such as the capital cost add-on for coal or explicit policies such as renewable portfolio standards. With the low cost for new facilities, natural gas shows the largest growth rate. Coal and nuclear remain essentially constant. There is modest growth in renewables.

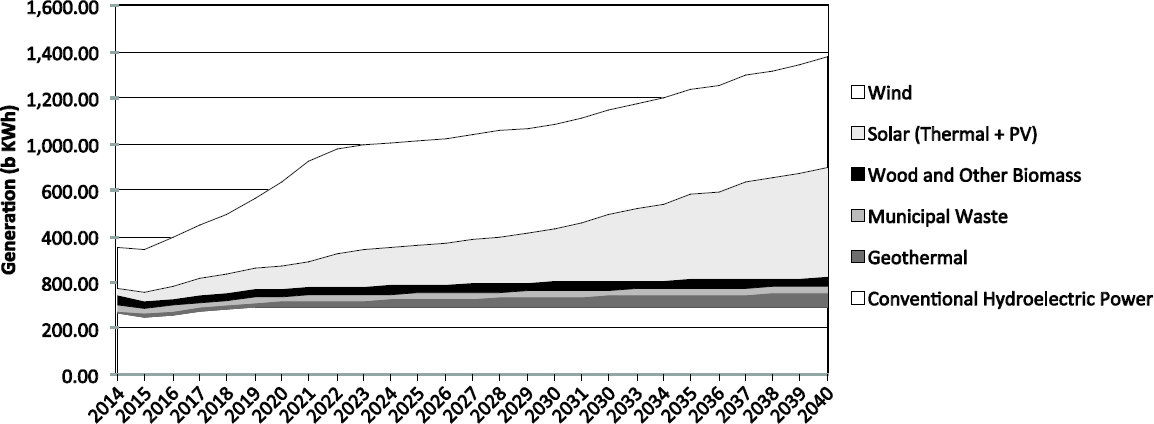

The breakout of the Reference Case projections for renewables shows that hydroelectric stays about constant, but the other renewables grow at modest rates (see Figure B-3). The penetration of renewables is important but substantially below the levels that would be indicated by an aggressive program to address remaining health effects and the challenges of global warming.

CONCLUSION

Equivalent estimates of the LCOE are available from the supporting analyses of AEO2016. The data without the effect of selective policies indicate that existing technologies for clean energy are not competitive with new natural gas. And without accounting for the costs of externalities, the principal renewable technologies of wind and solar are not cost-competitive with new coal plants.

SOURCE: EIA, 2016f, Figure IF3-6.

SOURCE: Renewable Energy Generating Capacity and Generation, Reference Case Tables (EIA, 2016a, Table 16).