3

Challenging Categories: Medical Care

In this chapter, the panel proposes a new way to more fully incorporate health insurance and medical care into a revised Supplemental Poverty Measure (SPM) which, for reasons explained in Chapter 2, is called the Principal Poverty Measure (PPM) in this report. Chapter 3 builds on the concept of a health-inclusive poverty measure and discusses measurement aspects and implementation decisions for putting the concept into practice. In the context of this chapter, the term “inclusive” conveys that—unlike the SPM—the PPM explicitly adds a need for health insurance to the threshold while “transfers” of health insurance, including those provided by the government and employers, are counted as resources.

3.1. BACKGROUND/MOTIVATION

The demand for medical care, unlike most goods, is uncertain. That is, while households can usually predict how much food they will need over the course of a month, this is far less true for medical care. Although individuals with chronic conditions will, on average, have predictably higher spending than those without such conditions, everyone faces the risk of unexpected illness or injury which creates unavoidable uncertainty about the need for medical care. While there is no way for individuals to insure their good health against the risk of unexpected medical events—that is, to guarantee that one’s underlying health status can be returned to its baseline level—individuals can insure against the risk of unexpected medical spending. Most individuals prefer to pay a predictable health insurance premium to mitigate the risk of unpredictable spending on medical care because they are risk averse.1 Nonetheless, most health insurance policies in the United States do not cover all costs of medical care: they require cost sharing in the form of copayments or coinsurance, such that consumers bear some of the costs of care (intended to deter unnecessary use of medical care).

Medical care expenditures are a large and increasing share of GDP (19.7% in 2020, up from 5.6% in 1965), with average per capita expenditures in 2020 equaling $12,530 (Catlin and Cowan, 2015; Hartman et al., 2022). Nearly 70 percent of this spending is financed by insurance (Hartman et al., 2022). The federal government spends more than $1.2 trillion annually on medical care—nearly all of it on insurance—accounting for more than 15 percent of federal outlays and dwarfing the next largest in-kind transfer program (the Supplemental Nutrition

___________________

1 Economists tend to view health insurance as providing protection against financial risk and value it as the expected loss in utility from the occurrence of adverse health events. Economic theory says that individuals are willing to pay a premium equal to that expected utility loss; a basic exposition can be found in the public finance textbook by Gruber (2022).

SOURCE: U.S. Census Bureau yearly SPM reports.

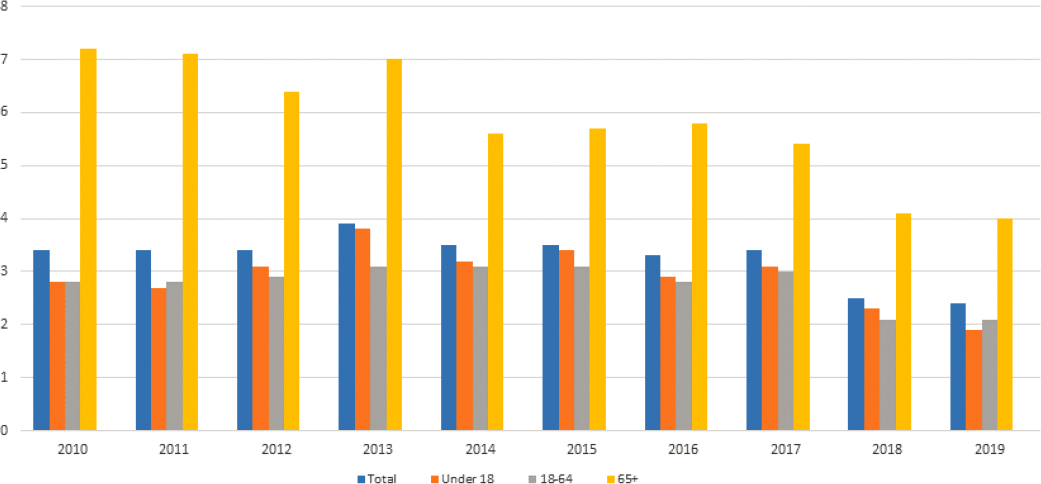

Assistance Program [SNAP]). The high level and rapid growth of health insurance and medical care spending underscores the importance of explicitly and accurately incorporating this basic need into the measurement of poverty. The 1995 National Academies of Sciences, Engineering, and Medicine report, Measuring Poverty: A New Approach (NRC, 1995), acknowledged the desirability of including medical care in the measurement of poverty but identified two key obstacles: variability in the need for care across the population, and the fact that health insurance benefits cannot be repurposed to pay directly for nonmedical needs such as food and housing. That panel’s compromise solution, reflected in the current SPM, was to deduct medical out-of-pocket (MOOP) spending on both health insurance and medical care from resources, without explicitly including a need for those goods in the threshold. MOOP expenses in the SPM include household payments for health insurance premiums plus household payments or copayments for other medically necessary items, such as prescription drugs, doctor visits, hospital visits, dental services, vision aids, medical supplies, and over-the-counter, health-related products that are not covered by insurance. As shown in Figure 3-1, accounting for MOOP expenditures in the estimate of a households’ resources typically raises the SPM poverty rate by about 3 percentage points overall; the increase is largest for those age 65 and older.

The current SPM approach likely understates the impact of government health insurance spending on measured poverty because the only channel through which these outlays can affect poverty is an indirect one—via the deduction of MOOP expenditures from resources.2 This fails to capture potentially important effects of government health insurance programs. For example, consider an uninsured individual who forgoes medical care entirely because of its high cost. If this individual gained Medicaid coverage that allowed them to obtain treatment, the SPM poverty rate would not fall. If this individual obtained subsidized coverage through an

___________________

2 As a reminder, the SPM income (resource) measure is cash income plus in-kind government benefits (such as SNAP and housing subsidies) minus nondiscretionary expenses (taxes, MOOP expenses, and work expenses). The SPM thresholds are based on a broad measure of necessary expenditures—food, clothing, shelter, utilities, telephone, and internet (FCSUti), but not health coverage—and are based on recent, annually updated expenditure data. The SPM thresholds are adjusted for geographic differences in the cost of living.

Affordable Care Act (ACA) Marketplace plan that allowed them to obtain treatment, their spending on premiums and copays would be deducted from their SPM resources, potentially pushing them below the poverty threshold and thereby increasing the poverty rate, as public subsidies for the purchase of coverage would not be counted as resources. These examples make clear that the treatment of health insurance and medical care by the SPM should be revised, if it can be done validly and practically. Specifically, a basic need for medical care should be included in the measure’s threshold and the value of transfers like Medicare, Medicaid, employer health insurance benefits, and health insurance premium tax credits in household resources. The approach described in this report offers a partial solution, proposing a method to incorporate health insurance into poverty measurement in a way that solves these problems, including modifying the SPM deduction from resources to incorporate the costs of medical care that are not fully covered by insurance.

3.2. TREATMENT OF HEALTH/MEDICAL CARE IN THE SUPPLEMENTAL POVERTY MEASURE: STRENGTHS AND LIMITATIONS

The current treatment of medical care in the SPM has advantages: it is relatively easy to implement, allows for a consistent expenditure-based definition of the needs threshold, and captures important effects of health coverage expansions via reductions in MOOP expenses.3 The SPM’s treatment of medical care also captures variation in spending that is driven by differences in medical care needs; holding insurance constant, households with higher needs will have higher spending. But the current SPM approach has three significant flaws. First, the value of health insurance provided by government or employers affects SPM poverty only indirectly, through its effect on MOOP spending. Second, because neither health insurance nor medical care are included as a need in the threshold, the SPM does not capture the unmet need for care of persons who are uninsured or underinsured. Third, the deduction of MOOP spending from resources is not limited, implying that all MOOP spending represents a “basic need” whereas, in reality, some MOOP spending on care or insurance cannot be accurately characterized as necessary expenditures. That is, the current approach implies that a family’s health need is simply equal to whatever the family spends out of pocket on insurance and medical care.

There are several alternatives to the SPM approach to medical care. Table 3-1 compares the Official Poverty Measure (OPM) and the SPM to four additional approaches found in the literature (for additional details, see Appendix 3A): (1) the health-inclusive poverty measure (HIPM; Korenman and Remler, 2016); (2) the SPM-MOOP in threshold (SPM-MIT) which, as its name suggests, includes a need for spending on health insurance and medical care in the threshold but may not capture the unmet need for those without insurance (Garner et al., 2014); (3) a two-index method which constructs a medical care economic burden and medical care economic risk index in addition to the nonmedical index (Institute of Medicine and National Research Council 2012b); and (4) the Full-Income Poverty Measure (FPM) which includes the value of health insurance transfers from government or employers in household resources; these values are also included in needs, to the extent that such transfers existed in 1963, because the distribution of the FPM in that year is used to define the initial FPM thresholds that are then updated for inflation (Burkhauser et al., 2020).

Among these alternatives, this panel’s preferred approach, described in greater detail below, builds on the HIPM developed by Korenman and Remler (2013, 2016) and Korenman, Remler, and Hyson (2019). The National Academies’ report Roadmap to Reducing Child Poverty recommended that relevant statistical agencies review the HIPM for adoption (National Academies 2019, Recommendation 9.8), and the Census Bureau has explored in depth the feasibility of implementing a health-inclusive concept in the SPM (Creamer, 2022). The HIPM approach, which explicitly incorporates the value of health insurance transfers into poverty measurement, builds on similar innovations in the SPM for incorporating other in-kind transfers.

___________________

3 According to the Social Security Administration, “MOOP is measured using the CPS/ASEC which collects information on amounts paid for (1) health insurance premiums; (2) over-the-counter, health-related products; and (3) medical care (hospital visits, medical providers, dental services, prescription medicine, vision aids, and medical supplies). Caswell and O’Hara (2010) concluded that CPS/ASEC estimates of MOOP expenditures compare favorably to estimates from the Medical Expenditure Panel Survey (MEPS) and the Survey of Income and Program Participation (SIPP). The MEPS, in particular, devotes considerably more effort to collecting MOOP expenditures than does the CPS/ASEC.”

TABLE 3-1 Six Approaches to Poverty Measurement and Their Treatment of Health Insurance/Care/Benefits/Costs

| Approach | Thresholds | Resources | Key References |

|---|---|---|---|

|

Medical care/health insurance not explicitly included in threshold | Medical care/health insurance not included in resources | |

|

Medical care/health insurance not explicitly included in threshold | Health insurance premiums and other household MOOP spending subtracted from resources | |

|

SPM thresholds, plus health insurance need | SPM resources, plus net health insurance transfers, minus capped nonpremium MOOP costs | |

|

Predicted MOOP spending included in threshold | SPM resources; MOOP spending is not subtracted from resources | |

|

SPM thresholds | Nonmedical: SPM resources, not subtracting MOOP spending Medical Care Economic Burden (retrospective): MOOP costs minus resources available for medical care (= excess of nonmedical resources over SPM threshold; zero for nonmedically poor) (separately for premiums and non-premium MOOP expenditures) Medical Care Economic Risk (prospective): Use burden measure as proxy until further R&D | |

|

Absolute thresholds fixed at the 19.5th percentile of 1963 “full income” distribution, which includes the value of health insurance transfers at that time; inflated using BEA PCE Price Index | “Full income” includes SPM cash and noncash income, plus health insurance transfers; no MOOP costs subtraction |

One challenge identified by the National Academies’ 1995 panel was that transfers of health insurance are not fully fungible. In the view of the current panel, the conceptual framework of the HIPM provides the best available solution. In particular, the panel prefers the HIPM-based approach to the approach used in the FPM which essentially treats health insurance benefits as equivalent to cash—that is, available to meet any need, medical or nonmedical. The FPM approach implies, for example, that a couple who receives Medicare is not poor, even if they have no other income or resources (Remler and Korenman, 2023); and, as a corollary, FPM poverty is reduced if prices for medical care rise due to increases in the cost of medications, for example, or an increase in useless procedures whose cost is counted as income to beneficiaries even if there is no change in real benefits to the patient (Case and Deaton, 2020). The panel also feels that the conceptual framework of the HIPM is preferable to that of the SPM-MIT as the latter implies medical care need is limited to MOOP expenditures. By excluding the value of health insurance benefits from resources, the SPM-MIT does not reflect the impact of public health insurance transfers on poverty estimates, such as those published annually in the Census Bureau’s SPM reports (e.g., Fox, 2020).

Finally, the HIPM approach has an advantage over the two-index approach in that the latter fails to capture how health benefits reduce poverty since medical care enters the measure as a separate index. The medical care economic risk index also employs complex imputations of health-related financial risk that require detailed information on health conditions and health insurance. While such information may be available in health surveys such as the Medical Expenditure Panel Survey, it is not collected in the social and economic surveys used to measure poverty (such as the Current Population Survey Annual Social and Economic Supplement [CPS-ASEC], American Community Survey, or Survey of Income and Program Participation). Research using this approach is valuable and could be particularly useful for understanding poverty of populations with special care needs and expenses, as well as the influence of new technologies on health-related financial risk. The poverty measurement approach proposed below does not adjust for individuals with special needs such as limited sight or hearing, or persons with other disabilities who may have health needs beyond those covered by health insurance, including Medicare. The recommendations discussed in this chapter are intended to improve the SPM by incorporating health insurance needs and benefits. They do not address other aspects of health or medical care. Clearly, research into other health care issues in poverty measurement should continue. But, at this time, the practical advantages of a health-inclusive poverty measurement approach for an official statistic that must be produced on a regular schedule are major and would increase the measure’s accuracy.

A critical assumption underlying the proposal for a PPM that is health inclusive is that the basic need for medical care has two parts: a need for health insurance and a need for resources to cover any required cost sharing. The basic need for health insurance can be represented by the price of an insurance policy: that is, the premium. As noted above, most individuals prefer to pay a predictable health insurance premium to mitigate the risk of unpredictable spending on medical care because they are risk averse. In economists’ terms, people willingly pay (and reduce current income by the amount of the premium) to avoid possible loss of far larger amounts if they need expensive medical care.4 Thus, the price of insurance—reflecting both the risk of needing medical care and the expected cost of that care—represents a large fraction of the health care need.

The insight that a substantial portion of health care needs can be represented by an insurance premium, combined with laws that require guaranteed issue and community rating of health insurance premiums, make it possible to incorporate a basic need for health insurance as part of the revision of the SPM to the PPM. Guaranteed issue means that health insurers cannot refuse to cover enrollees based on their health status, age, or gender while community rating means that all persons of a given age group face the same premium (and coverage) in a given market area. We find this logic compelling. But what premium should be used? The current ACA establishes a Marketplace along with an essential benefits package which meet these requirements. The essential benefits package includes a set of 10 categories of services that plans must cover including doctors’ services, inpatient and outpatient hospital care, prescription drug coverage, pregnancy and childbirth, mental health services, and dental care for children. To the extent that health insurance requires cost sharing, which the ACA benchmark plans all require, there remains a need for MOOP spending on medical care, which is addressed separately below.

RECOMMENDATION 3.1: For the Principal Poverty Measure, the current approach to medical spending in the Supplemental Poverty Measure should be replaced with one that includes health insurance in the estimates of both the needs threshold and resources.

The proposed approach within the PPM incorporates key modeling elements developed by Korenman and Remler (2016). As described below, one reason this innovation is possible is that the legal and regulatory framework of the 2010 ACA—namely, the specification of the benchmark health insurance plan and the requirement for community rating of premiums and guaranteed availability of coverage—dramatically simplify the process of specifying health insurance needs. “Benchmark plan” is the term used to describe the second-lowest-cost Silver plan available in the exchange. The benchmark plan also specifies an annual maximum for out-of-pocket spending on medical care (patient cost sharing), which can be used to limit (cap) subtractions from resources.

___________________

4 Risk aversion is tied to the concept of declining marginal utility of income so that the loss of a thousand dollars to a person with $15,000 “hurts” more than the same dollar loss to a person with $100,000.

3.3. INCORPORATING HEALTH INTO THE PRINCIPAL POVERTY MEASURE

As noted, the health insurance and medical care components of the recommended PPM would follow the HIPM approach (Korenman and Remler, 2016; Korenman et al., 2019). Specifically, the PPM would add the price of the benchmark health insurance plan (that is, the unsubsidized premium) to the poverty threshold to represent the health insurance need. The PPM would also add a value for health insurance benefits provided by government or employers to household resources, up to the price of the benchmark plan.5 Because the PPM threshold includes a need for health insurance, resources in the PPM do not deduct all out-of-pocket spending on insurance premiums. This is a departure from the SPM. As in the SPM, resources in PPM do include a deduction for medical out-of-pocket spending that is not on premiums, which we refer to here as nonpremium medical out-of-pocket (NP-MOOP) spending; unlike the SPM, the deduction of NP-MOOP spending is capped. Equations in Appendix 2A contrast the basic needs thresholds and resource estimation approaches as specified in the SPM and the PPM.

To address the remaining need for cost sharing, the PPM would deduct NP-MOOP spending, such as deductibles and copays, from resources. The deduction from resources is similar to the current SPM, but with two important differences. First, because a need for health insurance is explicitly included in the threshold and health insurance transfers are counted in resources, only out-of-pocket spending on medical care would be deducted from resources in the PPM; out-of-pocket spending on premiums by those who purchase health insurance directly from an insurer or on the ACA Marketplace is not deducted from resources in the PPM. Second, unlike the SPM, which allows an unlimited deduction for health insurance and medical care, the PPM would cap the deduction of NP-MOOP spending at the out-of-pocket maximum for ACA plans (or less, depending on the household’s health insurance type, as explained below). The conceptual justification for the NP-MOOP deduction is the same in the PPM as the SPM. Nondiscretionary spending on necessities not explicitly represented in the threshold reduces resources available to meet those threshold needs.

In the proposed PPM, unlike the SPM, the NP-MOOP subtraction is capped at available out-of-pocket maxima in the benchmark plan in an attempt to limit the deduction to spending that could be considered necessary. However, some spending below the NP-MOOP limit could also be for care that is discretionary, and some care above the maximum could be for nondiscretionary care. The PPM does not attempt to define or measure nondiscretionary spending below the out-of-pocket limit. The PPM procedure of capping the NP-MOOP deduction from resources is, therefore, a pragmatic compromise between the SPM assumption that all NP-MOOP spending is nondiscretionary and attempting to make judgments about whether specific medical care expenditures are or are not discretionary. If the health insurance plan included in resources were “full,” in the sense of not requiring any cost sharing, there would be no subtractions from resources for NP-MOOP expenditures.

There are other possible approaches to dealing with the remaining need for cost sharing. For example, the benchmark plan has an actuarial value of 70 percent, meaning that, on average, households will pay out of pocket for 30 percent of the cost of their care. The PPM could incorporate the need for cost sharing by inflating the benchmark premium to 100 percent of actuarial value and would make no deductions for actual NP-MOOP spending (Remler and Korenman, 2022). This method fully incorporates the average anticipated need for medical care into the need for health insurance. As noted by Remler and Korenman (2022), one drawback of such an approach is that it is based entirely on the anticipated, or ex ante, need for care as measured by the benchmark premium. Actual NP-MOOP expenses reflect the realized, or ex post, need for care. Some households, such as those including a family member with a disability, may consistently face higher than average NP-MOOP costs based on realized need beyond that reflected in their premiums. Others may have to pay considerable NP-MOOP costs in any given year due to serious injuries or other health shocks. Many, even most, people will be healthy in a given year and need substantially less than the average cost-sharing amount. Subtracting actual NP-MOOP spending (even capped, as proposed for the PPM) will capture these need-based differences in a way that the ex ante expected cost-sharing approach would not.

On the other hand, a threshold need that includes both the insurance premium and expected cost sharing would allow a more complete accounting of the impact of health insurance benefits on poverty. For example, Medicaid has

___________________

5 As envisioned by Korenman and Remler (2016), a health insurance sharing unit is a subunit of the PPM unit consisting of persons covered by the same health insurance policy (or policies), one of whom is designated by the CPS-ASEC as the policy holder. Poverty status is determined for each PPM unit (“household”) by aggregating resources and needs of the health insurance units to the PPM unit (household) level.

very low copays and would meet nearly all medical care and insurance needs. Employer-provided health insurance generally has an actuarial value higher than 70 percent and could be credited for meeting a larger portion of the full insurance-plus-care need.6

3.3.1. Threshold Health Insurance Need

That medical care is a basic need seems self-explanatory; the harder question, in terms of measuring poverty, is how much medical care should represent the modern standard. A key insight of the HIPM research is that a substantial portion of the basic need for medical care can be represented by the value of an insurance policy. In practice, this requires choosing an insurance policy to represent the basic need and, inevitably, not everyone will agree on which specific plan best represents the basic need. Because of differences in health insurance coverage options that depend on age and disability status, the policy that represents the basic need must vary based on those characteristics. For nondisabled individuals younger than age 65, the ACA benchmark plan presents a straightforward option for establishing the dollar level that should be added to the PPM threshold to reflect the need for health insurance. The ACA benchmark provides a practical and conceptually valid answer to the question: how much cash income would an uninsured person need to obtain a basic health insurance policy? Thus, in implementing the health-inclusive element of the PPM, the panel proposes adding the unsubsidized age-specific cost of the ACA benchmark Silver plan in an individual’s region to the threshold for individuals under age 65.7

RECOMMENDATION 3.2: For individuals under age 65 (excluding those who have Medicare due to disability), the Affordable Care Act (ACA) benchmark health insurance plan should be used to represent the basic health insurance need for a typical American household (or the designated resource-sharing unit for poverty measurement). The ACA defines a benchmark plan as the second-lowest-cost Silver plan available in the health insurance Marketplace in an individual’s geographic area. The Silver plan for those age 65 and over who are not covered by Medicare is also the basic health insurance need.

Using the ACA benchmark plans may limit the ability to construct a consistent pre-2014 historical series for the PPM. The panel recognizes this limitation but does not believe it is a strong enough reason to preclude recommendation of these revisions.

For Americans age 65 and older, as well as those who are younger but qualify for Medicare on the basis of disability, the threshold need for health insurance is defined as the full cost, including the government contribution, of Medicare, if the recipient were to choose the cheapest Medicare Advantage plan that includes a prescription drug plan (MAPD plan) available in their location (e.g., county of residence, if that information is available; if not, state of residence).

RECOMMENDATION 3.3: For the population age 65 and older covered by Medicare, as well as those under 65 who qualify for Medicare based on disability, the basic need level should be set based on the full cost of a Medicare Advantage plan that provides prescription drug coverage. The cost of this plan should be calculated as per-recipient federal spending on Medicare Parts A, B, and D, plus the lowest-cost out-of-pocket premium for the Medicare Advantage plan that includes a prescription drug plan.

As detailed below, the MAPD out-of-pocket premium is the additional premium required for the MAPD plan above the required Part B premium.

___________________

6 Remler and Korenman (2022) provide estimates and further discussion of these issues. They have not developed similar methods for incorporating Medicare, however.

7 Marketplace premiums may also vary by smoking status. The HIPM proposed by Korenman and Remler (2016) used the premium for nonsmokers. The PPM could allow the threshold need to vary by smoking status. The panel has not made a recommendation on this feature.

3.3.2. Resources

The National Academies’ 1995 panel, in discussing challenges to incorporating medical care in poverty measurement, highlighted the challenges associated with determining how much of the value of health insurance transfers should be considered fungible—that is, a resource that can be used to meet other needs. This panel shares those concerns and, therefore, the proposed PPM approach, like the HIPM, caps the value of the health insurance transfer included in resources at the amount included in the needs threshold. Thus, mathematically, the PPM approach to including these transfers in resources cannot lift an SPM-poor household out of poverty, since an equal or greater amount has been added to the threshold.

RECOMMENDATION 3.4: The definition of resources in the Principal Poverty Measure should include a value for any health insurance benefits or subsidies received from an employer or from the government but must also reflect the fact that such transfers cannot be used to pay for nonhealth needs. This is achieved by capping the value of the transfer that is added to resources at an amount that is less than or equal to the health insurance need that is added to the threshold.

Finally, NP-MOOP costs should also be deducted from resources, subject to a cap. This is similar to the SPM approach, with the addition of a cap for individuals who are not Medicare eligible. Starting in 2025, it will also be possible to cap the deduction for cost-sharing expenses for Medicare recipients, since the Inflation Reduction Act of 20228 caps prescription drug out-of-pocket spending at $2,000.9 The cap is operationalized by using the out-of-pocket limits specified in ACA Marketplace plans or other information about health insurance status and household characteristics. For example, many households covered by Medicaid with no cost sharing required would have their deduction for NP-MOOP spending capped at zero. This approach allows the PPM to capture variation in actual medical care spending needs associated with worse health status, as noted above, without implicitly deeming an unlimited amount of NP-MOOP spending to be necessary.

RECOMMENDATION 3.5: Medical out-of-pocket spending should be subtracted from resources in the Principal Poverty Measure. For individuals who are not covered by Medicare, this subtraction should be capped at the out-of-pocket maximum for Affordable Care Act Marketplace plans or lower, depending on health insurance status and other household characteristics. Out-of-pocket spending by Medicare recipients can also be capped starting in 2025, due to changes enacted under the Inflation Reduction Act, and the panel recommends doing so.

To give specific examples of how health insurance benefits and cost-sharing amounts are calculated for the resource measure, several illustrative scenarios follow (additional details of each are presented in Appendix 3B):

- For those with employer-sponsored health insurance, the value of the threshold need is added to resources as the health insurance benefit value (regardless of the actual value of their coverage). Reported out-of-pocket premiums paid by the household, capped at the value of the threshold need, are subtracted from the health insurance benefit value to form a net health insurance benefit amount. This amount—the benchmark premium minus capped out-of-pocket spending on health insurance premiums—is intended to stand in for the net value of the health insurance transfer from the employer. Reported nonpremium out-of-pocket expenses, capped at the benchmark maximum out-of-pocket expense, are also subtracted from resources.10 Hence, for a family with employer-provided insurance spending less than the caps, the family’s poverty status under the PPM and the SPM

___________________

8 See www.congress.gov/bill/117th-congress/house-bill/5376/text.

9 The $2,000 cap is adjusted for inflation annually after that time. In 2024, the cap will be $3,250, accomplished by eliminating the 5 percent beneficiary coinsurance requirement above the catastrophic coverage threshold.

10 Most employer plans have better coverage than the benchmark Silver plan, and lower out-of-pocket limits (benchmark out-of-pocket limits are quite high). The ACA defines minimum value for employer plans and if an employer does not offer a plan with minimum value, an employee can decline the employer plan and buy the benchmark Marketplace plan and get a premium subsidy, if eligible. If the employer offers a plan of minimum value that is “affordable” coverage as defined by the ACA, then the employee would not be eligible for subsidies for Marketplace plans. See, for example, Norris (2021).

- will be the same (see line 2a in both Panel 1A and 1B in Appendix 3B). Veteran’s Tricare is treated the same way. Those who are offered an employer plan but no subsidy (e.g., under COBRA) would have the benchmark plan value added to resources and a large premium payment subtracted, resulting in a zero health insurance benefit value. This process correctly shows that they will be poor if they lack sufficient cash income to meet the health insurance need in the threshold and the additional income and benefits to meet their other basic needs.

- For those with subsidized ACA marketplace coverage, the amount of the ACA premium subsidy is added to resources. Nonpremium out-of-pocket expenses, capped at the maximum out-of-pocket for the benchmark plan, are subtracted from resources.11 (See line 2c in Panel 1B in Appendix 3B.)

- Those with unsubsidized ACA marketplace coverage and those who buy insurance directly from an insurance company outside the Marketplace receive no health insurance transfer, and thus no net health insurance benefit amount is added to their resources, nor is out-of-pocket premium spending subtracted from their resources, since their need for health insurance is already captured by the need included in the threshold.12 Nonpremium out-of-pocket expenses, capped at the benchmark maximum out-of-pocket, are subtracted from resources (see line 2d in Panel 1B in Appendix 3B). Note that this is quite different from the way such a household would be treated in the current SPM, which does not include a threshold need for health insurance but would subtract all premium and nonpremium out-of-pocket spending from the household’s resources (see line 2d in Panel 1A in Appendix 3B).

- For those with Medicaid, the value of the threshold need is added to both the threshold and to resources. In most cases, no premium is required, and cost sharing is limited. But in cases requiring a small premium and/or cost sharing, these are deducted from resources.13 The panel considers this to reflect incomplete insurance so, consistent with those getting a subsidy to purchase coverage on the Marketplace, cost sharing is taken as a reduction to resources, while the value of Medicaid is added to resources. For those covered by VA Health Care, the approach is the same.

- For those with Medicare, to form a net health insurance transfer value, the value of the threshold need is first added to resources. Recall that threshold need value is defined as equal to the full cost of Medicare: actuarial value (per-beneficiary federal spending on Medicare Parts A, B, and D) plus the lowest-cost MAPD out-of-pocket premium in the county of residence. For the net transfer value, the beneficiary’s required Part B premium is then subtracted from resources, as is additional reported premium spending, capped at the lowest-cost MAPD additional premium amount. (The Part B premium is zero for those with incomes below 132% of the federal poverty level.) To capture the need to pay for cost sharing, nonpremium out-of-pocket expenses are also subtracted from resources, and for Medicare beneficiaries, there is currently no cap on the amount that may be subtracted.14 This will change in 2025, when a cap will apply to Medicare beneficiaries; at that time, Medicare beneficiaries should be treated consistently with the approach recommended for those with employer coverage, other private coverage, and ACA coverage, in which NP-MOOP expenses are capped.

- For those with no health insurance, nothing is added to resources. Nonpremium out-of-pocket expenses, capped at the benchmark maximum out-of-pocket, are subtracted from resources.15 The logic behind this

___________________

11 For those eligible for ACA cost-sharing subsidies, the PPM nonpremium MOOP costs cap is lowered according to a sliding scale based on income.

12 Those able to purchase a plan as a result of the ACA do benefit from the existence of an ACA Marketplace and from community rating and guaranteed issue, but if they do not qualify for a subsidy, they must still have sufficient cash income to purchase the benchmark plan.

13 Medicaid NP-MOOP amounts could be capped either using state-specific policy parameters or, more simply, at 5 percent of income according to federal requirements.

14 An MAPD plan was chosen as the threshold need plan for the PPM (and the HIPM before it) because these plans limit out-of-pocket spending on medical care. However, MAPD plans have not limited out-of-pocket spending on prescription drugs (those with very high expenditures may pay 5% copays on marginal expenditures). If the CPS-ASEC collected separate spending amounts for out-of-pocket spending on medical care and prescription drugs, the medical care portion of the cost-sharing deduction could be capped. Moreover, due to Medicare changes in the Inflation Reduction Act, out-of-pocket spending on prescription drugs will be capped at $3,250 in 2024 and $2,000 in 2025 and indexed thereafter (Cubanski et al., 2022). Thus, the deduction from resources for cost-sharing expenses for Medicare recipients in the PPM should also be capped beginning with calendar year 2024.

15 Uninsured individuals are matched to a benchmark plan, based on individual characteristics and geography, to determine the maximum out-of-pocket payment.

- approach is that a person should not be deemed poor if they have sufficient resources to meet their nonhealth needs, purchase the benchmark plan, and pay for their medical cost-sharing expenses up to the maximum out-of-pocket limit under the benchmark plan. If an uninsured person spends more than the maximum cost-sharing amount out of pocket, such expenditures would be considered discretionary in the sense that they could have been avoided by purchasing the basic insurance plan and are therefore capped at the out-of-pocket maximum. While there is room for debate on this point, the approach reflects a consistent and practical choice for determining a basic need for medical care for the purpose of poverty measurement.

3.3.3. Future Considerations

The proposed approach raises three questions that the panel leaves for future research: (1) How should free and reduced-price care be incorporated into poverty measurement? (2) Does poverty measurement—either the SPM or the PPM—adequately account for the greater needs of households that include individuals with disabilities? and (3) What happens to PPM poverty if there are changes in the policies on which this approach implicitly relies (specifically, the specification of a benchmark plan, and its guaranteed availability at a community-related premium)?

On the first question, regarding free care: conceptually, free and reduced-price medical care should be counted as a resource for households that use it, or households that have the option of using it. For example, one might impute a resource value reflecting the availability of free care from a Federally Qualified Health Center in a given geographic area.16 At this point the panel does not recommend including free care in the measure, but suggests that free care, as well as reduced-price care, be studied in the future.

On the second question, the panel deems it important to study ways to better incorporate the needs of individuals with a variety of disabilities into the measurement of poverty. These needs may include specialized equipment, aides, housing modifications, and counseling—many of which are not covered by health insurance. Research should continue to develop ways to incorporate these needs, both medical and nonmedical, into poverty measurement. In the panel’s opinion, this is not a reason to defer the adoption of the PPM to improve the accuracy of poverty measurement.

Finally, what happens to PPM poverty if there are changes in policy? Changes in the benchmark plan—for example, revisions over time to the generosity of coverage—are likely, but they present no methodological challenge since the PPM incorporates these changes into both resources and needs. More problematic would be changes in the ACA guaranteed issue and community rating regulations, since these are required for the determination of the threshold health insurance need specific to each household. Without guaranteed issue, there is no assurance that a person with a given amount of income could purchase an insurance policy that meets their basic health needs. Without community rating, insurance premiums could once again depend on detailed health characteristics (e.g., preexisting conditions), and determining the basic plan premium would require access to the detailed health information and actuarial models used to set private insurance premiums. Indeed, this would represent a return to the conditions that led the National Academies’ 1995 panel to exclude health needs and health insurance benefits from the recommended approach that became the SPM.

In this chapter, the panel’s case has been made that the Census Bureau should move forward with development of a PPM that incorporates an explicit need for health insurance in the threshold, adds the value of health insurance transfers to resources, and modifies the deduction of MOOP spending from resources so that only nonpremium MOOP expenses are deducted. Medical care is a major component of individual spending, whether directly or in the form of health insurance. It is a major and growing component of the U.S. gross domestic product. Medicaid and Medicare are by far the government’s largest in-kind transfer programs, and health insurance is the largest nonwage benefit provided by employers. To accurately measure poverty, it is necessary to include the need for care and the value of these transfers. This chapter describes the best way to do so, using the framework of the health-inclusive poverty measure. The panel recommends that the PPM incorporate this approach.

___________________

16 Korenman et al. (2018) present estimates using alternative approaches to incorporating implicit insurance values of free care to the uninsured in HIPM estimation for the state of New York.